September 23, 2022

Remember last year’s blogpost where we asked whether the Fed was really serious about tackling inflation? Well, since then Chairman Powell has been taking pains to demonstrate that yes, he is serious. Very serious. So, let’s talk another look at the question.

Chair Powell has certainly been talking the talk, saying in a speech at the Jackson Hole central banking conference that the Fed’s commitment to price stability is “unconditional”. Just to make the point clear, he warned that tackling inflation would cause pain but argued that a failure to to restore price stability “would mean far greater pain”.

At the same time, he has been walking the walk, taking out the heavy artillery for the fight against inflation. Over the past few months, he has been firing especially large shells:

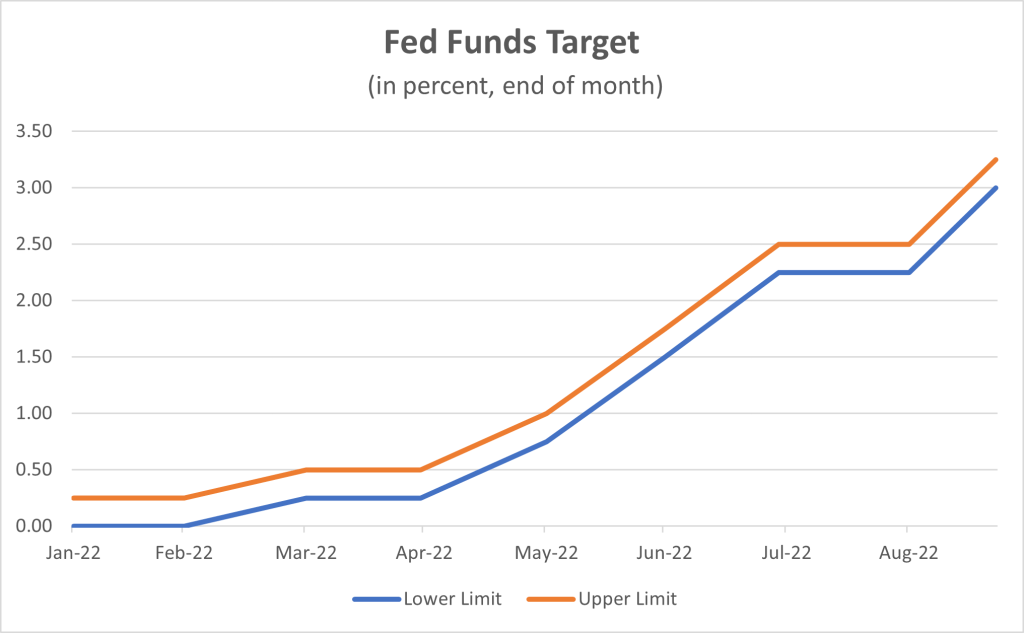

- In June, it raised interest rates by 75 basis points (0.75 percent). Thud.

- In July, by another 75 basis points. Thud.

- And yesterday, by yet another 75 basis points. Thud.

In all, rates have been increased five times so far this year, by a cumulative 300 basis points. The Fed’s target rate is now around 3 percent, the highest it has been in one and a half decades.

And the Fed plans to keep firing its artillery for some time. Every time the Federal Reserve Board meets, members make projections of where they think Fed interest rates will need to go over the next year. During the September meeting, most of the members projected that its target rate (the “Fed Funds” interest rate) would rise to 4.6 percent by 2023, in order to ensure that inflation was well and truly vanquished.

So, that’s it, right? The Fed is on the job. So we can all stop worrying about inflation.

Oh, dear. If only it were that simple.

Start with the magnitude of the problem. Again and again, most forecasters have underestimated the tenacity of the price increases. Last year, they argued that inflation was transitory, the result of pandemic-induced supply constraints that would surely fade away as soon as Covid ebbed. As a result, the Fed confidently assured us, inflation would fall to 2 percent by the end of 2021.

But their diagnosis was wrong: inflation was caused by too much demand, not by a collapse in supply. And so their prediction was wrong: inflation hit 7 percent by the end of last year, not 2 percent.

But that didn’t stop “Team Transitory”. Instead, they started to argue that inflation was concentrated in just a few items, like oil prices, so once the prices of these items normalized, inflation would fall rapidly. Well, they were right about oil prices: the international price of crude has plummetted to around $90/barrel from a peak around $120/barrel. But inflation? Um, not so much. Inflation remains 8.3 percent, higher than it was at the beginning of the year.

The news gets worse. The standard way to assess the underlying trend in inflation is to look at “core” inflation, which strips out the influence of oil and other goods whose prices are volatile. It turns out that core inflation is stuck around 6 percent, far higher than the Fed’s target of 2 percent. In other words, in this case, the trend is not the Fed’s friend. That means the Fed will need to exert some effort to get inflation back down.

But isn’t that exactly what the Fed has been doing? Well, yes and no. Yes, the Fed has been increasing its interest rate. But no, rates are still well below the underlying inflation rate: 3 percent, compared to a core inflation rate of 6 percent. Put another way, real rates are negative. And negative real rates give an incentive for people to go out and spend money, rather than keeping it in the bank. Which in turn fuels more inflation.

There are only two basic ways out of this situation. Either inflation finally does fall of its own accord. Or the Fed will have to keep raising interest rates — perhaps beyond 6 percent, far above what it is envisaging today — until rates turn positive in real terms. (Of course, some combination of these two outcomes is also possible. But let’s keep the analysis simple.)

Now, we come to the heart of the problem. It’s just not clear whether the Fed has the ability or even the willingness to do what it takes to defeat inflation.

Why would the Fed be unable to defeat inflation? Well, because the Fed — like everyone else — is fallible. And it is especially fallible in the current circumstances, because it has never experienced an economic situation like the one it is now facing.

Just consider the current circumstances. For the past two quarters, the US economy has been stagnating. Yet the number of jobs has been growing rapidly, and demand for workers remains about twice as large as the number of people looking for work. A stagnating economy, where it is really easy to find a job? No one has seen anything like it. How will this play out? No one knows.

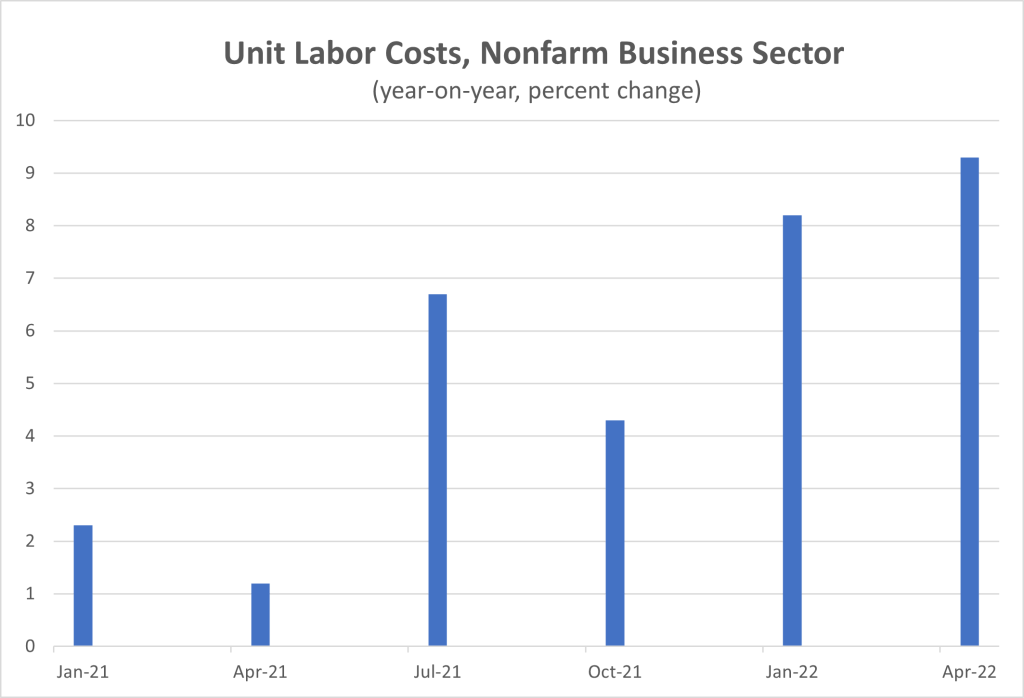

Consider another conundrum. In recent quarters, labor productivity — meaning the amount of output that each worker produces per hour — has suddenly started to fall like a stone. Why would worker productivity be falling? No one knows. Will it continue? No idea.

All this matters immensely to the inflation outlook. Let’s say that the current situation continues. That is, employers remain so determined to hire workers that they increase wages, in order to convince people who weren’t planning to work to go out and get jobs. Meanwhile, labor productivity continues to fall.

In that case, firms’ costs will soar. After all, if wages per hour increase while the amount of production per hour (productivity) falls, then wages per unit of goods produced will rise sharply. As they have been doing.

If firms’ costs continue to rise sharply, inflation will continue to run rampart, because firms will pass on these costs into prices. Which means that workers will demand wage increases to preserve their standard of living. Which means that firms’ costs will go up again. And so on.

Of course, the opposite could also happen. Firms could decide that they need to be cautious and stop offering higher wages to hire workers. Meanwhile, productivity growth could go back to normal. In that case, unit labor costs could ebb, in which case firms would not face so much pressure to raise prices. Then, inflation could fall.

So, there are (at least) two plausible scenarios. Does the Fed know which one will materialize? No, it does not. And therefore it doesn’t know how aggressive it needs to be in raising interest rates. If it raises rates aggressively, when firms are already cutting back on their hiring (the second scenario), then it could send the economy into a tailspin. But the same amount of interest rate increases could be vastly insufficient to quell inflation if the first scenario materializes.

All of this means that the likelihood of the Fed making a mistake is exceptionally high. But what kind of mistake? Put another way, if it is going to err, will it err on the side of ensuring that price stability is restored? Or will it be timid, keeping interest rates low, out of fear of causing a deep recession?

Chairman Powell insists that he will not make the second mistake, since he is focused exclusively on price stability. And so far this year that is indeed what he has been doing. Thud. Thud. Thud.

But he really be able to maintain this focus? There are reasons for doubt. Consider just one piece of evidence. On September 7, Jason Furman published an article in the Wall Street Journal entitled The Scariest Economics Paper of 2022. Now, who is Jason Furman, you ask? Well, he is a very sensible economist. He teaches at Harvard, he was the head of the Council of Economic Advisors under President Obama, and — most importantly — he has been warning for some time that inflation is going to be a big problem. So, if anything, he would seem to represent the faction of economists that argues that the Fed needs to be aggressive, in order to get prices back under control.

But what does he argue in the op-ed? He notes that some economists have written a paper arguing that unemployment will need to rise sharply before inflation gets under control. I won’t go into the details of the paper. Suffice to make two points. One, that the paper is based on an empirical model. And we all know that empirical models have not had a good track record recently, because ultimately they are based on past experience, whereas the current economic situation has been truly, strangely, confusingly exceptional.

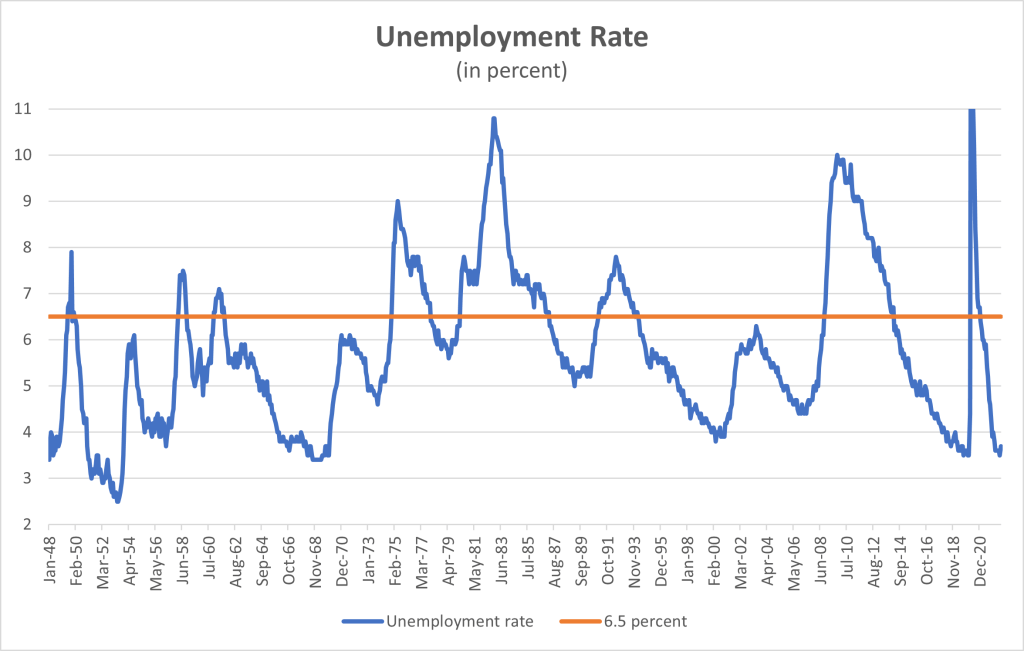

But even if the model does “work” in the current circumstances, what does it actually predict? Well, Furman calculates that getting inflation down to 2 percent would require squeezing aggregate demand so badly that unemployment rises to 6.5 percent. And he finds that prospect truly scary.

Wait, what? It is true that an unemployment rate of 6.5 percent would be considerably higher than the current rate. And higher unemployment is never a good thing. But 6.5 percent unemployment is not an exceptionally high rate. The US has faced it in the past, many times. See the graph below (where I’ve cut off the pandemic peak, because it was literally off the charts).

Serious recessions — like the ones in the early 1980s and late 2000s — are associated with much higher unemployment, around 10 percent. So, double-digit unemployment is certainly scary. But 6.5 percent? Um….

The point is this. If even moderate, sensible economists such as Jason Furman are warning that the pursuit of price stability would result in a “scary” level of unemployment, would the Fed really have the courage to take this path?

In the Christian Bible, there is a story about Christ and Saint Peter. After Christ is crucified, the saint decides to flee Rome, so that he can save his own skin. He is walking along the Appian Way when suddenly he meets the risen Christ. Startled, Peter asks, “Quo Vadis?” — which way are you going? Christ responds, “I’m going to Rome to be crucified again.” Ashamed, Peter turns around and goes back to Rome, where he too is crucified. (There’s a famous 1951 film of the same name that examines this period, under Emperor Nero. But I digress.)

The Fed now faces a choice. Is it really willing to choose the path of inflation control, knowing that it may be “crucified”? Or will it bow to those who say that such a path is too scary and choose the same path as in the 1970s, where it took a full decade for the Fed to summon enough courage to raise real rates to the levels needed to conquer inflation?

Quo vadis?