Last week, Leslie Lipschitz and I wrote a column for Barron’s, where we warned that the Fed could not remain passive in the face of mounting inflation. It needed to come out with a credible plan to bring inflation back to 2 percent – and it needed to do so quickly. Right on cue, the Fed yesterday announced what the press is calling the Powell Pivot. After many months of dismissing the current inflation as “temporary”, Chairman Powell finally banished the t-word from his lexicon and announced instead moves to tighten the monetary stance.

So, there we have it: finally, the big move to tackle inflation. But there’s just one nagging thing. Normally, when the Fed signals that it’s going to be raising interest rates, the stock market sinks. And yesterday, the stock market reacted by….soaring. The S+P 500 rose by 1.6 percent, its biggest one-day rise in more than a year. So, um, what exactly is going on here?

One possibility is that markets were reassured that the Fed was finally acting to address the inflation problem. But there is another possibility.

It’s not often that “pivot” is used to discuss monetary policy. More often, it’s used in sports like basketball. And there, we know exactly what it means. Typically, when the guy with the ball suddenly pivots, he’s just doing a head fake, designed to make you think he is going in one direction, when he is really going in another. So, before we jump to conclusions about the direction of monetary policy, we need to ask: is this the big move…or just a head fake?

To answer this question, we need to look at the details. Or as they used to say on the sports shows, “Let’s go to the video tape.”

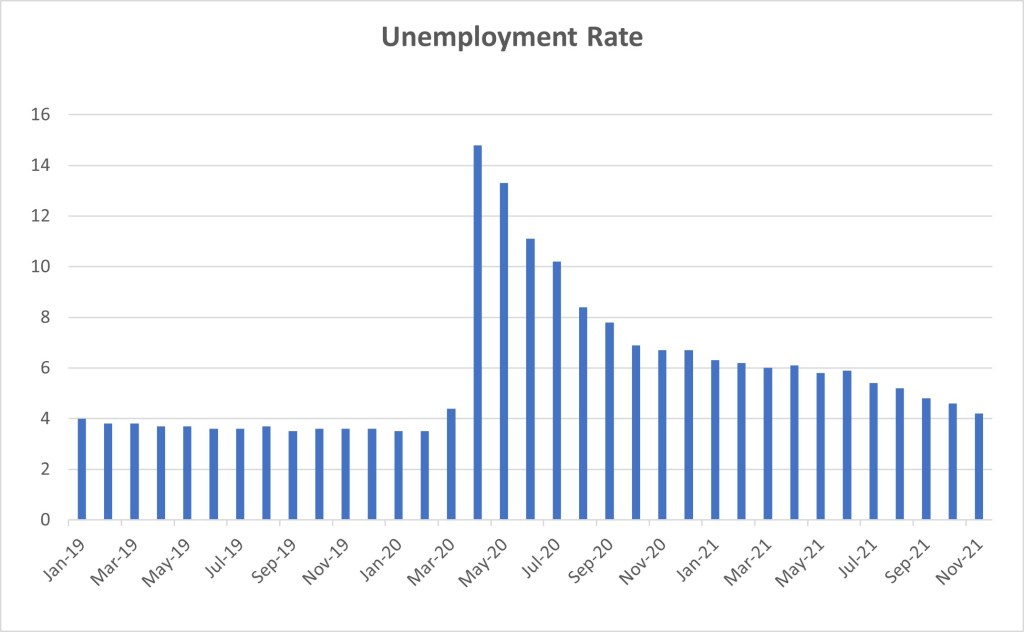

For those of you who haven’t been paying close attention, let’s quickly summarize the game so far. Even though waves of Covid keep coming at us, the economy is recovering nicely. Unemployment, which had soared to more than 14 percent at the peak of the lockdowns, has now fallen back to around 4 percent, pretty much where it was when the pandemic started.

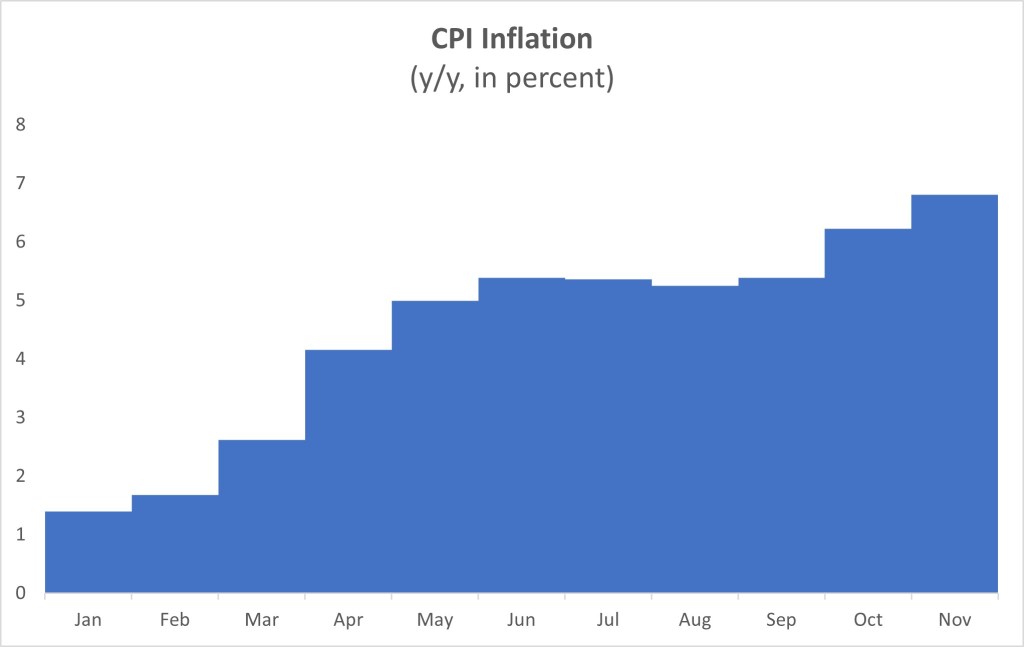

But inflation has not been performing as nicely. It has been marching higher, reaching 6.8 percent in November, the highest it has been in nearly 40 years.

As this march has gone on, for month after month, the public has begun to suspect that the inflation is not “temporary”, the way Fed Chairman Powell predicted in April. Instead, it could be a major shift in our economic environment: the end of long era of price stability.

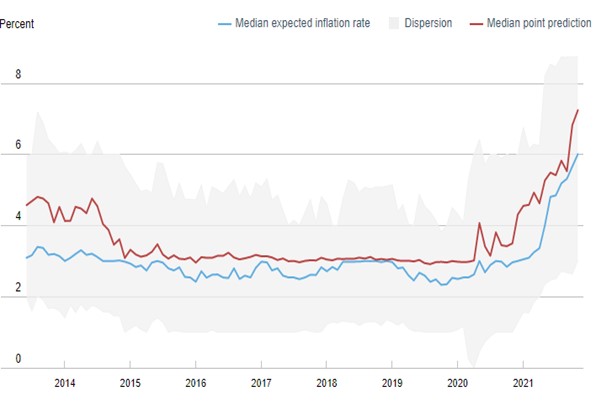

Every month, the New York branch of the Fed surveys consumers to find out what they are thinking. For years, they have given the same response: inflation will remain low over the coming year. But recently they have changed their minds: they now expect inflation to be high, around 6 percent. This is a serious problem, because once firms start planning price increases and workers start demanding compensating wage increases, it will be very difficult for the Fed to halt this process. That’s why it needs to act quickly.

What specifically should the Fed do? Well, normally it would say something like this: we are determined to bring inflation back to 2 percent over the next year or so, and to do this we will be increasing interest rates so that we can curb demand, which is running far ahead of available supply. Then, the central bank would indicate how high interest rates will need to go to achieve its target.

Instead, the Fed issued the following statement. “With inflation having exceeded 2 percent for some time, the Committee expects it will be appropriate [to maintain interest rates around 0 percent] until…labor market conditions have reached….maximum employment.”

Wait, what? Inflation is at nearly 7 percent, unemployment is low, firms are begging for workers and the Fed is worried…that there aren’t enough jobs? Really?

What is going on here?

Well, one possibility is that the Fed is just trying to reassure people who worry that it will focus exclusively on inflation, rather than on helping the recovery along. So, let’s ignore the rhetoric and look at what the Fed said it actually plans to do.

The Fed said that it plans to end Quantitative Easing, its strategy of buying bonds to inject cash into the economy, by the end of March. But this just means that it will be taking its foot off the gas pedal. That’s very different from saying it will start applying the brakes to inflation. To apply the brakes, the Fed will need to start raising interest rates. To explain why, I’ll need to get a bit technical. But hang in there. It’s really not that complicated.

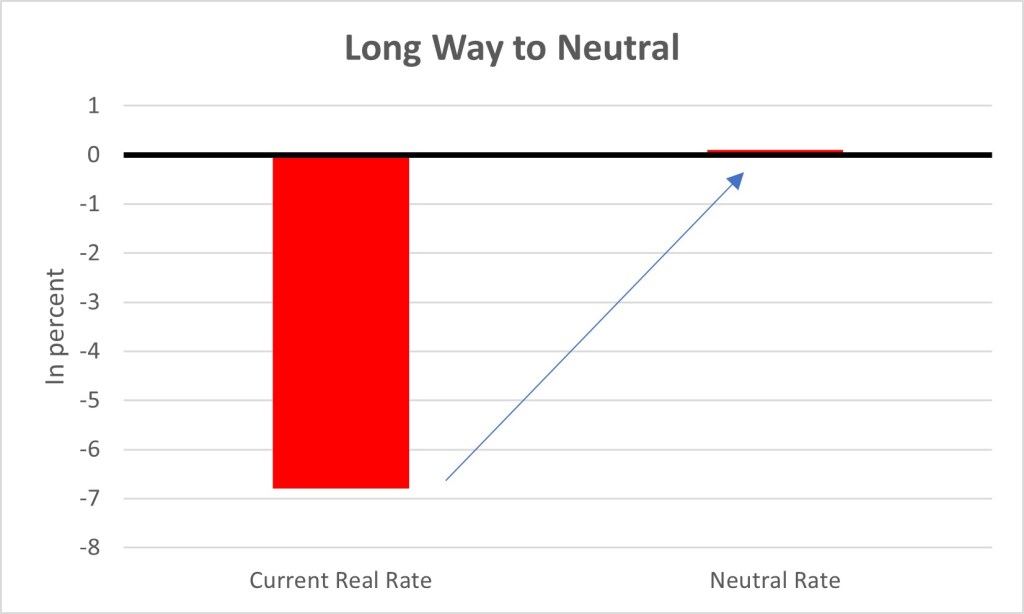

All central banks have a notion of a “neutral” interest rate, that is an interest rate which is, well, neutral for the economy. That is, if the central bank pegs interest rates below the neutral level, it is trying to stimulate demand. And if rates are higher than that level, it is trying to curb inflation. Of course, the level of the neutral interest rate is a subject of much academic debate. But a reasonable guess is that it is somewhere around 0 percent in real terms, meaning the nominal rate less inflation.

Right now, the Fed’s nominal policy rate is around 0 percent, implying that once you take inflation into account, the real interest rate is deeply negative. That means the the Fed needs to increase interest rates just to stop stimulating the economy and get monetary policy back to neutral.

So, what is the plan? The Fed doesn’t actually announce what it intends to do. Instead, it indicates what the individual members on its policy committee think would be appropriate. Their ideas for the next year are as follows, as measured in basis points (bp, 1/100 of a percentage point):

• 1 member sees only one 25 bp increase in the Fed Funds rate

• 5 see two 25 bp increases

• 10 see three 25 bp increases

• And 2 see four 25 bp increases

That is, even the most aggressive member of the committee is only thinking about raising the policy rate to 1 percent, by the end of the year. That would still be an historically low interest rate, likely to be negative in real terms and so lower than the neutral rate. In other words, even the most hawkish member of the Committee is saying that monetary policy should be expansionary at this juncture.

So, now we can see why the stock market is celebrating. The Powell pivot is nothing more than a head fake. As with basketball players, the artistry is impressive. But how exactly will this get inflation under control?

The Fed might have banished the word “temporary” from its press statements. Clearly, though, it is still betting that inflation will vanish of its own accord. This is a huge, consequential bet. We can only hope that it is right.