One day, you are sitting at home, relaxing after another ordinary day. Everything seems so familiar, so comfortable. The couch, kitchen table, bed. They’ve all been around for so long that it’s difficult to imagine what life was like before they were there. It’s all so….reassuring.

But the next day you wake up, and suddenly everything seems to have changed. All the old familiar landmarks have gone and been replaced by….what, exactly? You look left. You look right. Everything seems so strange; nothing seems to make sense. Where on earth am I?

Actually, this question is easy to answer. You are in the land of stagflation. You can see with your own eyes that it’s a desolate land, marked by the ruins of previous civilizations. Amazingly, some very old people have actually been to this land, and they can tell you some amazing stories….about 20 percent interest rates, 10 percent unemployment, and housing costs so high that people need to take out mortgages that lasted 30 years or more.

It’s all very disconcerting. Two thoughts occur to you, and start buzzing round and round your head. How did we get here? And are we only paying a short visit, or have we been condemned to stay in this forsaken place for a long, long time?

Answering these questions will take a while, several blogposts in fact. So, strap on your backpack and let’s get started.

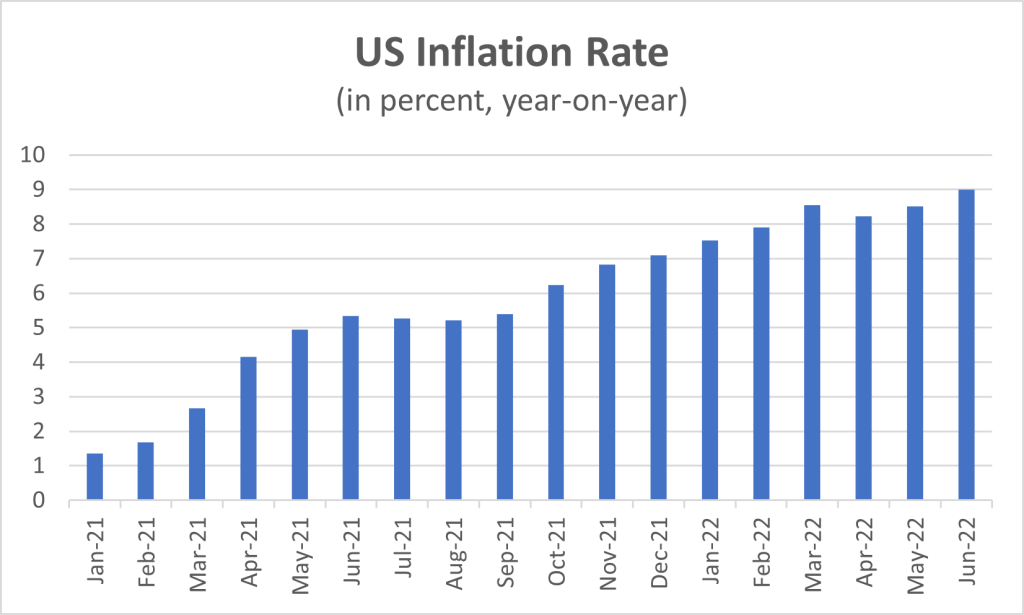

Start with the inflation problem. As you can see from the chart below, inflation started to rise in early 2021. When this occurred, there were a few people who argued that this was a bad omen of things to come. But most people argued that the inflation was transitory, caused by the pandemic lockdowns that were constraining production. These people were consequently sure inflation would disappear in a few months, as soon as production chains normalized. Indeed, the US Federal Reserve was so confident of this assessment that it projected that inflation would be back to 2 percent by the end of 2021.

We now know that the Fed was wrong. Inflation has not dissipated — it has continued to rise, reaching 9 percent by June. So what is going on?

Most people tell the following story. The initial assessment was fundamentally correct. It’s just that two unexpected things happened. First, Russia invaded Ukraine (“Putin’s War”), causing the price of energy to skyrocket. And second, it turns out that restoring the supply chain is far more complicated than initially thought. Even now, it is difficult to find new cars to buy; the automobile companies still can’t produce many cars because there’s still a shortage of computer chips. And even simple products are amazingly difficult to obtain. Try ordering some windows for your house. Or (until very recently) getting infant formula.

The implication of this story is that we just need to be patient. Energy prices will not rise forever. Indeed, they have already begun to ease, falling for a barrel of West Texas crude from a peak of around $120 in early June to less than $100 today. Similarly, the supply chain problems will eventually be resolved.

But we need to be careful here. There is much loose talk of a “supply chain crisis”. But what exactly is the evidence for such a crisis? In fact, when you look at the data, evidence is surprisingly sparse.

Let’s start with the data on US industrial production. As you can see from the chart below, production fell sharply during the lockdown in the spring of 2020. But by the end of the year it had largely recovered. And now it has surpassed its previous peak. So, um, why are we still speaking of production problems?

Perhaps, you say, because there is such a thing as a supply chain? After all, everyone knows that much (most?) of the goods consumed in the US aren’t actually produced in the US. They are produced in China. And in China, as everyone also knows, lockdowns are not a thing of the past. They are still a current-day reality.

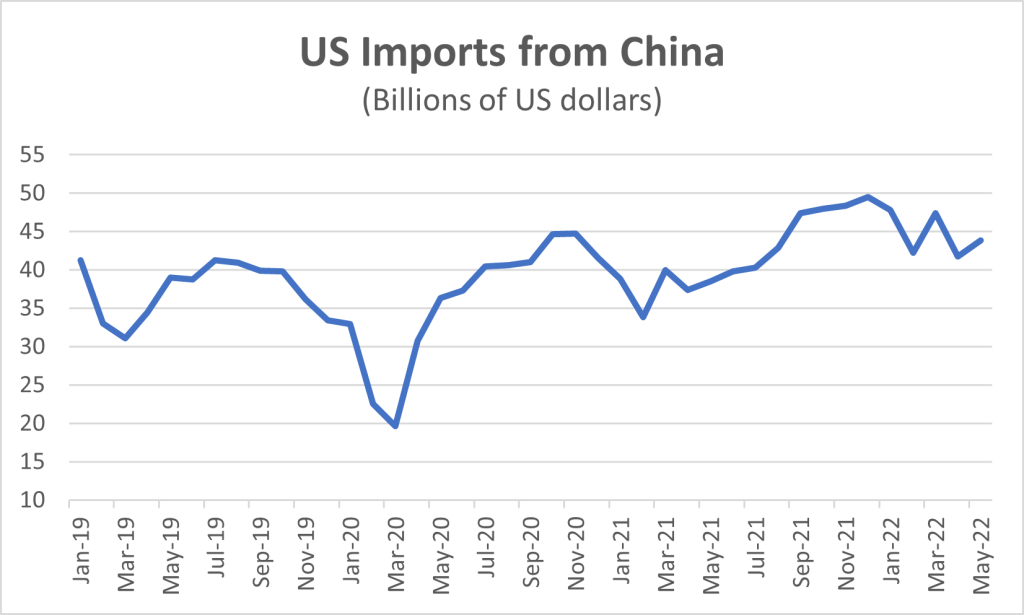

So, let’s take a look at Chinese exports to the US. Here, the pattern is similar to US industrial production, but with one pronounced difference. As in the US, there was a collapse in shipments during the US lockdown period. But afterwards exports rebounded smartly. By July 2020, they were back to pre-pandemic levels, and they have generally remained above those levels ever since.

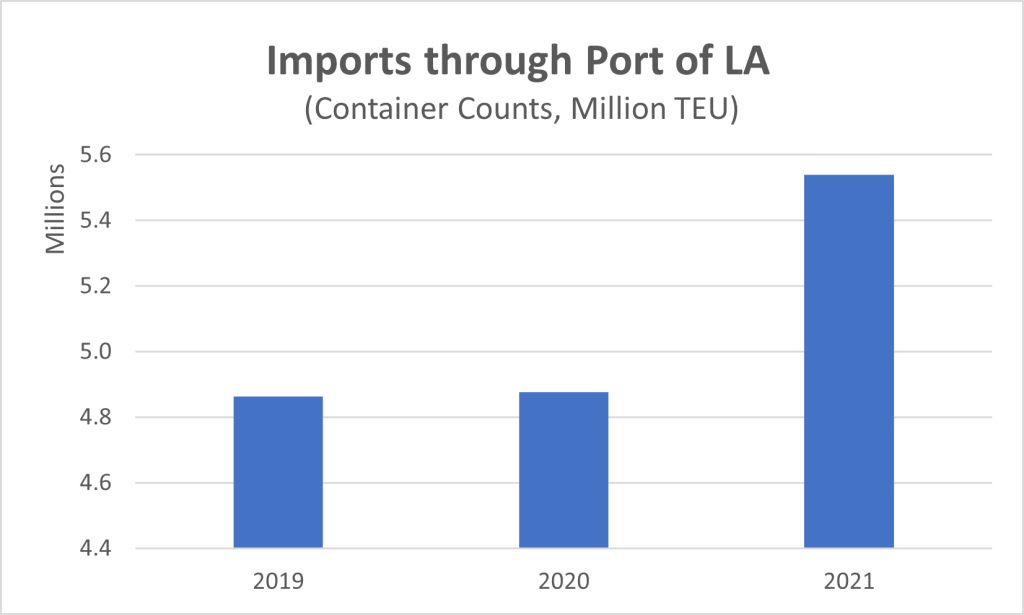

But wait, I hear you say, what about the shipping problems? Everybody knows that shipments were tied up forever at the port of Los Angeles. So, sure, China may have shipped the goods, but did they actually arrive in the US?

If that’s your question, then it is worth clarifying that imports mean….imports. That is, the US Customs only records a good as imported when it actually arrives in the country. But sure, just for the record, let’s take a look at traffic through the port of Los Angeles. (This also has an advantage, because LA handles goods coming from all over Asia, not just China.)

I’m pretty sure that you’ve never actually seen this data, because all those articles about the problems at the port never seem to have shown a chart about what actually was happening there. So, let me be the first.

Here it is.

See the problem? Neither do I. The graph clearly shows that imports were about the same in the pandemic year of 2020 as they were in the previous year. And in 2021 they hit a record level.

So, no, apart from the few months of US lockdown, there was no collapse of the supply chain, at least not in the sense that there was a fall in the supply of goods. But then what happened? Why were there shortages of products? And why has inflation taken off?

For the answers to the questions, you’ll just have to wait for the next posts. Because if there’s one thing that is correct about the conventional wisdom, it’s that we really do need to be patient!

See you soon.