October 19, 2022

Many years ago, there was a comedian named George Carlin. Nobody talks about him nowadays, but in the 1970s he was big. Really big. And the reason he was really big was that he was willing to say things that no one else wanted to say in public.

His most famous routine was called Seven Words You Can Never Say on Television. It wasn’t based on actual experience. He didn’t even try to say these words on TV. But one day a New York station dared to broadcast his routine on the radio. Right in the middle of the afternoon. Furor ensued, which eventually led to a case in the Supreme Court, which confirmed that the FCC indeed had a right to keep these words off the airwaves.

Fast forward exactly 50 years. Times have changed. But there are still some words that you are not supposed to say in polite company. Today’s list is somewhat different, of course. Some of the words that Carlin used have lost their power to shock, but new words are constantly being added to replace them. For most of the past year, for example, you just could not mention the R-word. It was just not done.

This was made clear by none other than the President of the United States. In July 2022, after a disappointing GDP report, some people started to use the R-word to describe the US economy. But almost immediately President Biden intervened to put a stop to this loose talk. “The US is not in recession,” he said, sternly. And if a recession does come, he said recently, “it will be a very slight recession.” So, to use one of the few New York expressions that you can mention in polite company, “fuhgeddaboudit!” And by and large, most polite people did.

Until now. Just over the past few days, something has changed. Suddenly, the taboo has vanished and the R-word is on everybody’s lips. The Wall Street Journal published a poll, which showed that a majority of economists now think a recession is likely. At the same time, Bloomberg sent an even stronger message. It published a piece saying that the chance of a recession is precisely…100 percent.

So, now that the taboo has been broken, let’s address the issue. Is the US barreling head-first toward recession? And what about that claim that we are in a recession, already?

We’ll get to these questions. But let’s begin by stepping back a bit. In essence, what the R-worriers are saying is that the Fed is making a horrible mistake by raising interest rates, because this is going to drive the country into recession. So, to evaluate their claim we first need to understand what the Fed is actually trying to do.

Let’s start with a really simple example. Let’s say that you have some money, which is burning a hole in your pocket. And you have a great idea of how to spend it: you want to go out to that hot restaurant just around the corner. But when you phone them up, you find out that all their reservations are booked. And when you complain, they tell you that the problem is that they are really short-staffed, so they have had to cut back on their hours, which means that they just don’t have that many reservations to give out. But of course, they understand that you are a really great person, so yes, they will give you a table…if you are willing to pay for the reservation. (You think I am kidding? Nope.. I kid you not. Read this article from the New York Times.)

In other words, when there is high demand and tight supply, prices are going to go up. How can this terrible situation be resolved? Well, one part is obvious: supply could improve if the restaurant can find some more staff. But the other part is less obvious, namely the role that the Fed can play. The answer is that if the Fed raises interest rates, you might decide that it is more rewarding to save your money, rather than spend it at that expensive restaurant. So: reduce demand, improve supply, and — hey, presto! — inflation problem solved.

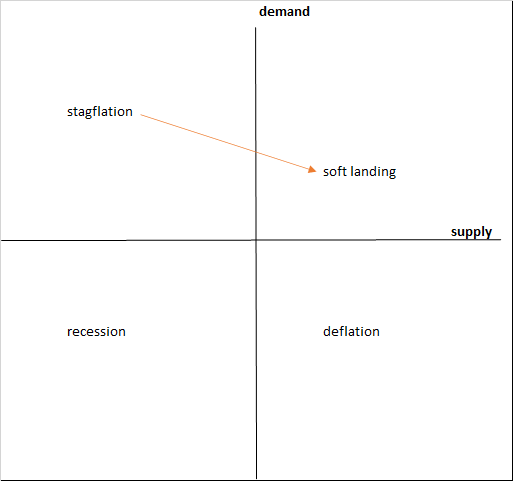

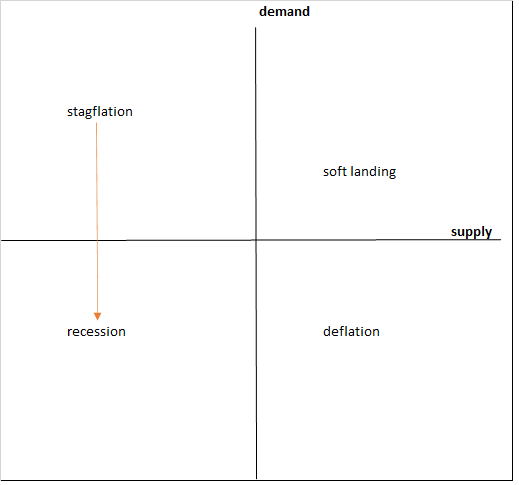

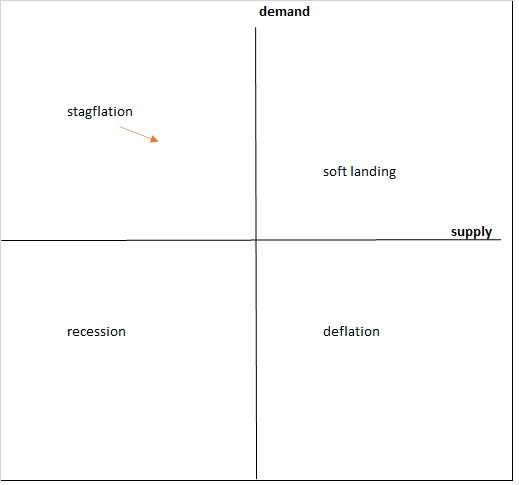

We can visualize the Fed’s strategy by considering the following diagram. It shows four quadrants, based on the strength of aggregate demand and aggregate supply. Right now, we are in the northwest quadrant, where demand is strong but supply is weak. Since demand exceeds supply we have inflation. And since supply (of workers and hence output) is weak, the economy is stagnating. There’s a technical term for this: stagflation.

The Fed’s goal is to guide the economy to the northeast quadrant, where demand and supply are in better balance. The idea is to raise interest rates to trim demand, while waiting for supply to improve, as people go back to work and bottlenecks disappear. If this scenario materializes, inflation will subside and growth will re-accelerate. The technical term for this happy outcome is: a soft landing.

Of course, if the Fed doesn’t guide the economy properly, the US could end up in one of the other quadrants. But, hey, the Fed has plenty of experience doing this monetary policy stuff. So, what could go wrong?

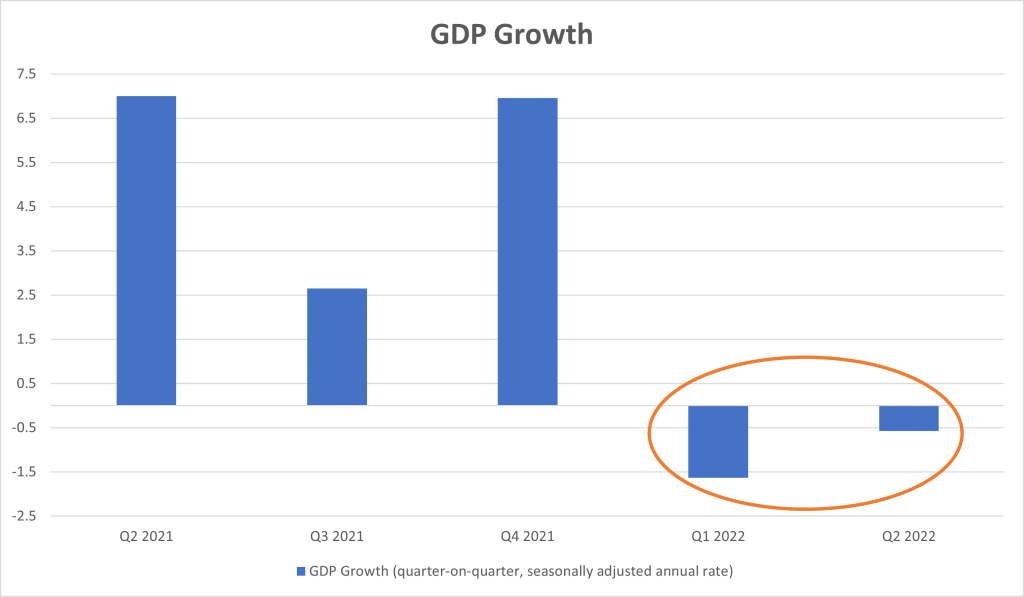

Um, plenty. The first problem for the Fed is that it doesn’t have a firm grasp of the current situation. It’s not really their fault, because the current situation is, well, confusing. As you can see from the chart, the economy has now contracted for two consecutive quarters. And yes, normally that is pretty much the definition of a recession. So, yes, President Biden was engaging in politics when he denied this claim. That, ahem, is what politicians do.

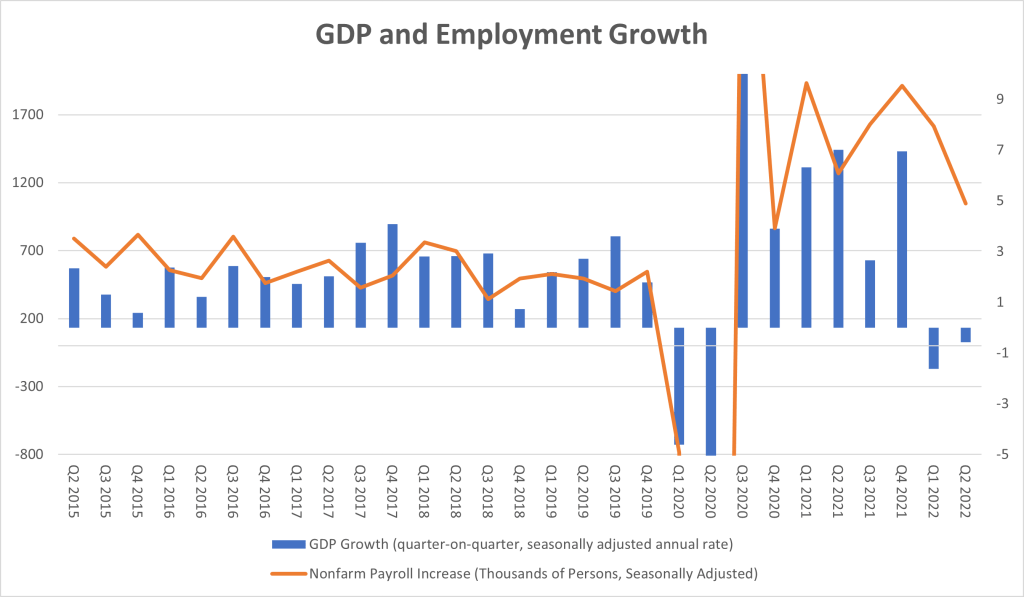

But the President had a point. The reason why most people just look at GDP as an indicator of economic health is that normally all the other things that we care about, like jobs, are highly correlated with GDP. Consider the following graph of GDP growth and employment. If you look at the left hand side, you can see that two move closely together. Employment quickens when the economy is growing and turns negative when the economy contracts. This makes sense, right?

But lately this nice correlation has broken down completely. Look at the right hand side of the graph. You can see that the economy is contracting (blue line)…but employment is somehow still growing (orange line). Not just by a little bit. By a lot. Much more rapidly than a few years ago when the economy was expanding robustly. Um, this makes no sense. No sense at all.

And that poses a big question. Is the economy weak, as the GDP figures suggest? Or is it strong, as the employment numbers imply? It is difficult for the Fed — or for anyone else — to say.

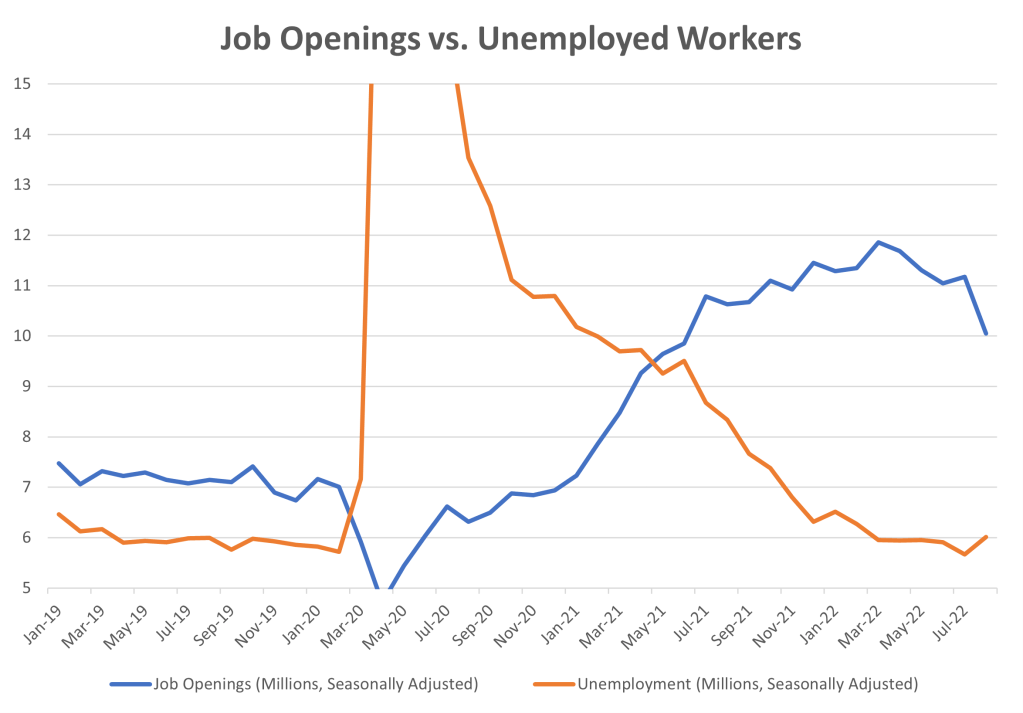

Now, consider the outlook. Perhaps the best way to think about things is to consider the following chart. Again, focus on the right-hand side. You can see that job openings (blue line) are at an exceptionally high level. In other words, employers are desperately looking for workers. But there are relatively few people looking for work (orange line).

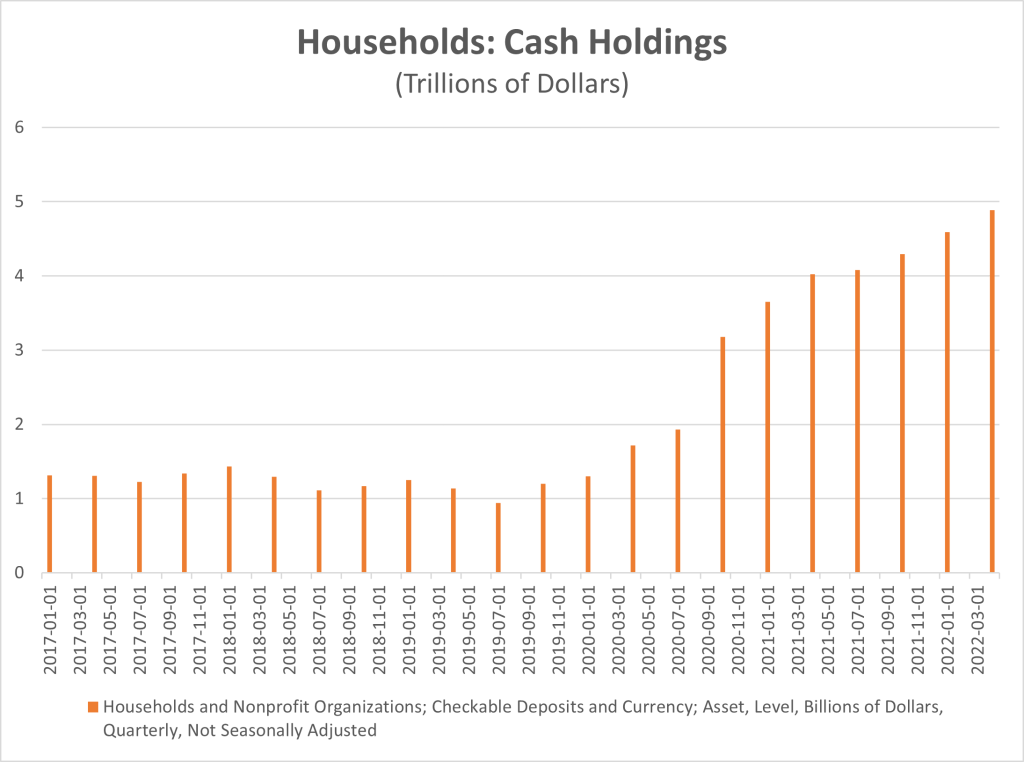

Why are relatively few people looking for work? The truth is that we don’t know the answer. But we have a few clues. One is that people are still sitting on a lot a cash, which they accumulated when the government kindly sent them a series of checks during the pandemic. Most people don’t know how large this stimulus really was. So, take a look at this chart of cash holdings, by which I mean actual cash plus the money in checking accounts. You can see that before the pandemic households had been holding around $1 trillion in cash. But then came the stimulus checks and suddenly these holdings quadrupled to $4 trillion, and then quintupled to $5 trillion.

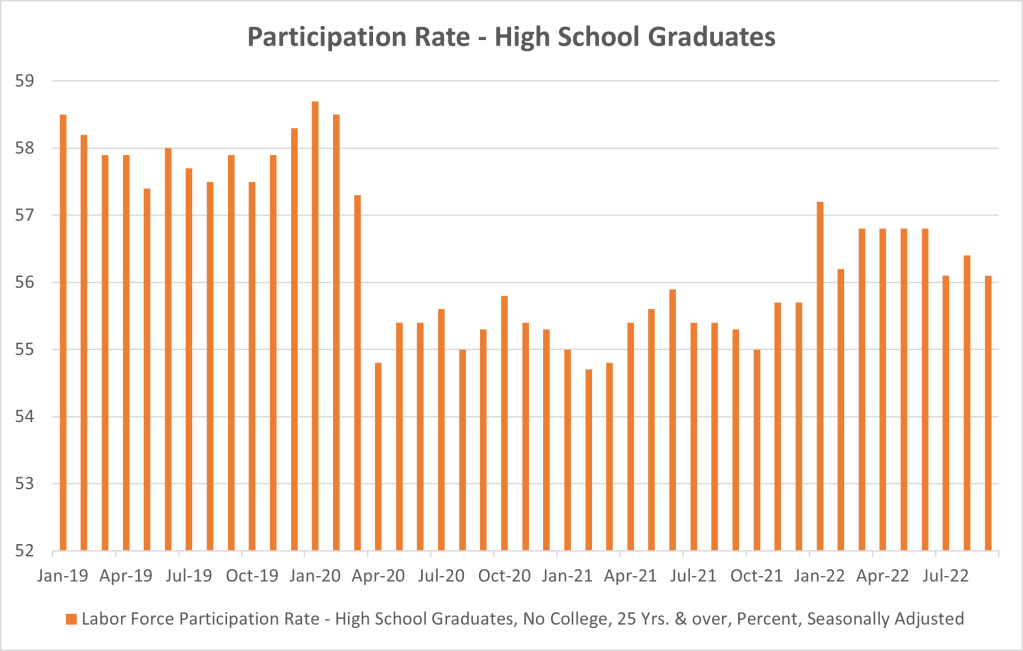

So, consider the case of a married couple, both high school graduates, who typically work at minimum wage-type jobs. Right now, there’s just not a huge pressure on both of them to go out and earn more money. That’s why a lot of them have just not gone back to work in restaurants and shops.

There are two ways this situation could play out. If the US is lucky, the people who left jobs during the pandemic and are still staying at home could eventually decide they are willing to go back to work. In that case, the economy could roar ahead, as businesses staff up and expand their activities. For example, restaurants could finally restore normal operating hours. (I hope!) Let’s call this the “strong economy” scenario.

Alternatively, employers could just give up looking for workers and scale back their expansion plans. In that case, the economy will continue to stagnate. Let’s call this the “weak economy” scenario.

Which one of these scenarios is going to materialize? No one knows, because no one has any experience with such a situation. An economy where employers are desperate for staff but can’t find enough people who want to work? No one has ever seen such a thing. So we have no idea how it will play out.

Are you keeping count? So far, we have mentioned two, ahem minor, problems for the Fed. One, the current situation is murky. Two, the outlook is cloudy. And we are still not done. There is yet another problem: the Fed has no idea how its interest rate increases will affect the economy.

In fact, it’s possible that the Fed’s tightening has been far too aggressive, and is going to drive the economy into recession. Why would this happen? Consider that the Fed has raised interest rates by a huge amount, three full percentage points in just a few months. And this rapid increase is forcing a huge adjustment on the economy.

For the past decade and a half, the economy has been built around the premise that interest rates were low (essentially, zero) and would stay low indefinitely. In such circumstances, it made sense to borrow as much money as possible and invest it wherever there might possibly be a positive return. Tech startups. Emerging markets. Peleton shares. Whatever.

But now that interest rates have increased substantially, this game is now over. And that is creating some pretty sizeable consequences. Consider the stock market. As investors have pulled their money from the market, prices have plunged, erasing some $15 trillion — that’s trillion with a “t” — in wealth. In addition, the rate increases have put pressure on the banking system, with the major banks all declaring large falls in profit in the September quarter. The rate increases have also led to a strong US dollar on the foreign exchanges, which will hurt the profitability of US exporters.

So, households, banks, and exporting firms are all getting squeezed. That’s a fair portion of the overall economy. And as a result, there is a risk aggregate demand and aggregate supply could both collapse, pushing the economy into the dreaded southwest quadrant, where a deep recession awaits.

Case closed? Not quite. Consider the argument on the other side. This argument starts by claiming that that the economy is actually much stronger than the “recession-istas” think: otherwise, how can you explain all those job offers? Obviously, firms think that business is good and going to get better — if only they can convince more people to come back to work. And things will indeed play out this way, since people can’t sit on the sidelines forever. At some point, they will run out of savings and need to earn some money. That means the “strong economy” scenario is the most likely one.

Moreover, the risks of transition from zero interest rates are overstated. Unlike in 2007, when the financial system was dangerously exposed to subprime bonds, banks have learned their lesson and been much more cautious in recent years. So have firms. So have households. All now have very strong financial positions, so they can easily withstand higher interest rates. For example, while the stress has reduced the earnings of banks, the level of profits still remains quite high. So, it’s highly unlikely that we will see the bankruptcies that we saw during the Global Financial Crisis.

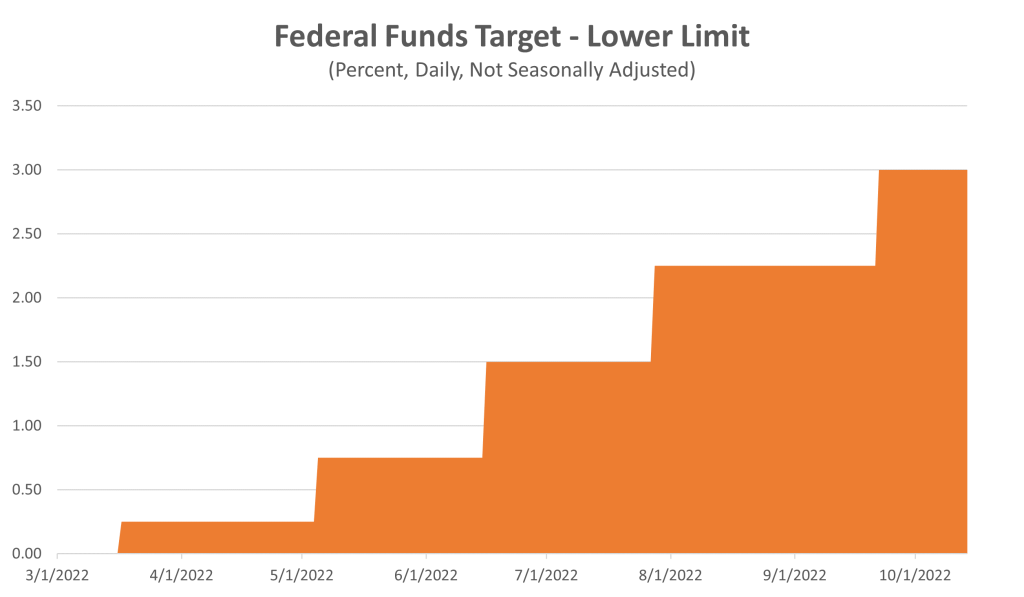

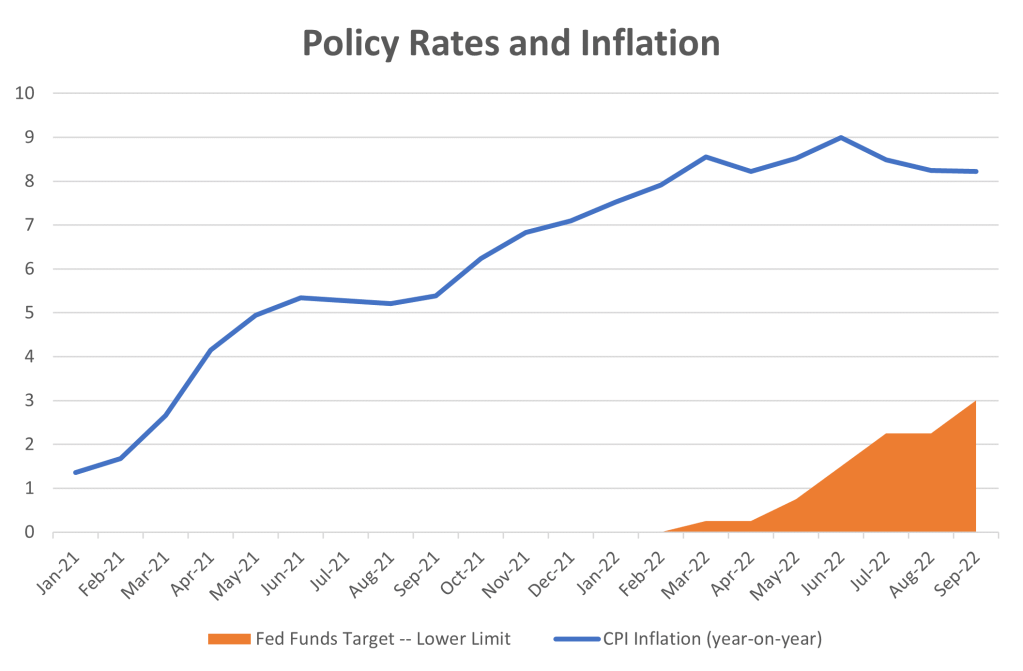

Finally, the Fed’s medicine is actually much more mild than the recession-istas allege. You can see the point from the following chart. Inflation took off in the spring of 2021. But the Fed did not start raising interest rates until a full year later. Even then, the interest rate increases have not come anywhere close to matching the increase in inflation.

Ah, so the economy is not heading for recession, after all! After all that fretting, it turns out there’s nothing to worry about!

Well, not exactly. Let’s say that the “Fed is being really prudent and is only administering some mild medicine” argument is correct. But let’s follow that logic to its proper conclusion. If the medicine is so mild, then how can we be sure that it is strong enough to get rid of high inflation?

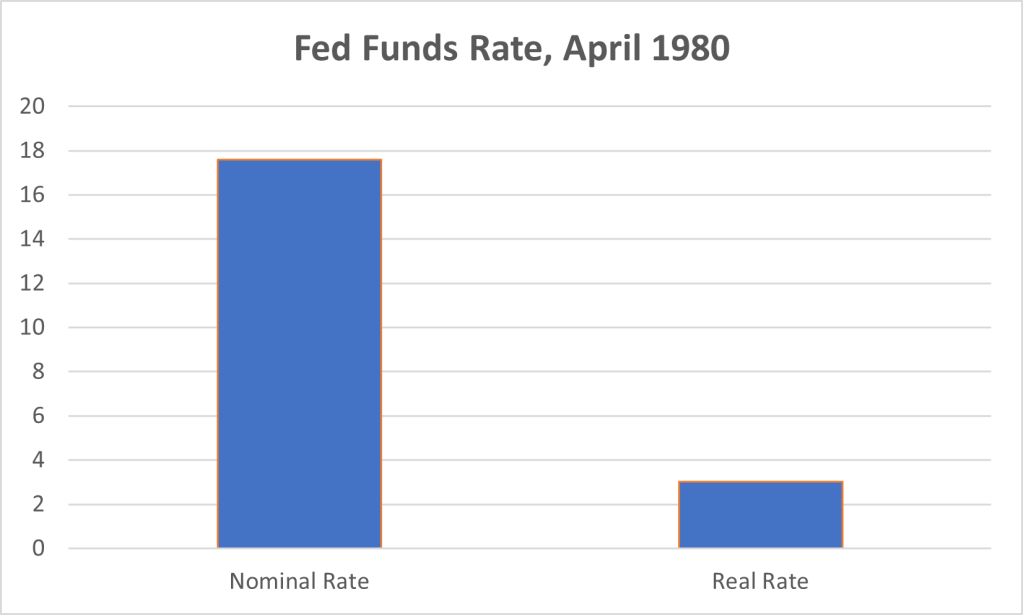

The answer is….we can’t. If we go back in history, we see that it has actually taken some pretty strong medicine to defeat inflation. For example, the last time that inflation was this high — 40 years ago — then-Fed Chairman Paul Volker needed to raise nominal interest rates to pretty high levels, well above inflation to squeeze price increases out of the system.

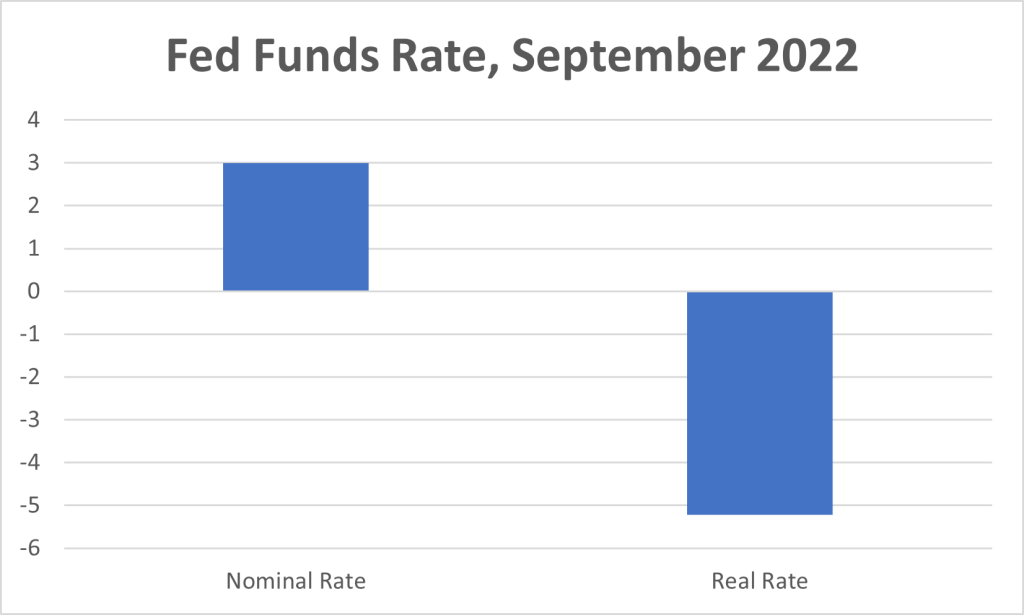

No one is saying that interest rates need to be that high today. For a start, eradicating high inflation in the 1980s was particularly difficult because it had been entrenched in the system for more than a decade. In the current case, high inflation has only been plaguing the country for the past year. That said, it remains true that by normal standards, Fed rates still seem, um, a bit low.

And if the Fed keeps interest rates too low — say, because it is afraid of causing a recession — then the US might remain pretty much where it is now, with high inflation and a stagnating economy.

To sum up, the Fed has a problem. Three problems, in fact. It doesn’t know where economy is right now. It has no idea where the economy is heading. And its steering wheel is broken: it doesn’t know how its interest rate changes will affect the economy. In other words, the Fed is flying blind.

In these circumstances, the chance that the Fed is going to steer the plane exactly where it needs to go — that is, to administer precisely the right amount of interest rate increases — seems pretty small.

Instead, the Fed is likely to make one of two mistakes:

- If the “strong economy” scenario materializes and the Fed’s actions have little effect on demand, the US might remain mired in stagflation. Just like the 1970s.

- Alternatively, if it turns out the US has a “weak economy” and the Fed’s tightening imparts too much stress on a system built around zero interest rates, the economy could collapse. Just like in 2008.

Either way, the landing is unlikely to be a soft one. Rather it could look something like this:

There’s a technical term for such a prospect. But I won’t tell you what it is. Because it’s one of the original Seven Words You Can’t Say on TV.