Did the Budget Hit the Bulls Eye?

July 23, 2024

What should we make of the new Budget? Well, if you listen to the commentators on TV, they will all tell you that it was a “9 out of 10, possibly even a 10 out of 10.” Then, they will give you a long list of measures that they liked in the budget, along with an impressive-sounding explanation of why they liked these measures.

You know the drill. Something along the lines of, “Well, the FM adjusted rule 10.27, which effectively reduced the tax on widgets from 30 percent to 29.5 percent, which is a major, major change that is bound to spur a boom in the widget industry and generate crores of new jobs. So, this is a major, major measure, indeed.”

By the end, after listening to all the many lists of the many, many major measures, your head is swimming in details, none of which you can remember. The only thing you know is that experts have assured you that the budget is a 10 out of 10. Just like the previous budget. Just like every budget that has ever been presented, none of which (or virtually none of which) have ever really solved the country’s economic problems.

So, let’s proceed with a different approach. Let’s evaluate the budget not by making a list, but rather by creating a framework. And I’ll be brief here, because really the last thing anyone needs is yet another commentary that will make your head swim. I’ll just stick to a few big points.

Why do we need a framework? Well, obviously, because it simplifies things. But beyond this, because you cannot really evaluate a budget unless you have some defined criteria. Two criteria, in particular. The first question is: has the government recognised the major problems that the country is facing? And if the answer is yes, the second question is: are the policy prescriptions likely to solve these problems, or at least ameliorate them?

Start with the question of whether the budget addressed the major challenges. The recent national elections showed that the electorate was worried about the lack of jobs, rural distress, and food inflation. Since the last two are related (in the sense that higher agricultural production would improve farm incomes and bring down food prices), for simplicity let’s just lump these two issues together under the heading of rural distress. In addition, there’s the long-standing problem that the government’s deficit is far higher than the 3 percent of GDP ceiling mandated by the Fiscal Responsibility and Budget Management (FRBM) Act. So there were three major problems that needed to be addressed.

Did the Budget address them? Yes, it did. The budget placed considerable emphasis on all three issues. So it did well on the first criterion.

As for the second criterion, perhaps it’s too soon to tell. After all, much depends on the details of the schemes and the effectiveness with which they are implemented. But already there are some reasons to wonder.

For a start, because they are schemes, not policies. That is to say, there’s no overarching change that would alter the policy framework in which all firms and individuals operate, as Arvind Subramanian and I advocated recently. The government did not set out an economic vision, much less a policy strategy to achieve it. Instead, it offered narrowly targetted programs, designed to alter certain incentives of certain firms and individuals. Will this approach really work?

Consider the Employment-Linked Incentive schemes. The key fact to note is that the government is planning to spend Rs 2 lakh crore over 5 years on these programmes. In other words, Rs 40,000 crore per year. In the grand scheme of things, this is not much money. It just isn’t enough to make a major dent in the employment problem, not in a country of 1 1/2 billion people.

But perhaps the incentive effects might be so powerful that a little bit of money will go a long way? This doesn’t seem likely, either. Consider the programme that the government thinks will have the biggest effect on employment, Scheme A. This scheme offers Rs 15,000 in the first month (only) to new workers who have found formal sector jobs. On the face of this, the incentive seems odd. In the current environment, getting a formal sector job is like winning the lottery. Why should anyone be rewarded for winning the lottery?

Now, it’s possible that the subsidy will actually end up going to the employer. That is, the employer might simply say that if an applicant wants to get a job, he (or she) needs to hand over their Rs 15,000 bonus. In that case, the scheme would indeed give an employer an incentive to hire some new workers. In principle.

But this seems doubtful in practice. The amount involved is just too small. Rather, what seems likely is that firms that were planning to hire workers anyway will apply to the scheme, and collect money for doing things that they were planning to do all along. Employers might even think of more “creative” scenarios. These possibilities will put tremendous strain on the government to monitor the scheme carefully, to ensure it is not being abused.

What about the agricultural schemes? Again, the amount of money is not particularly striking. If you add up the allocations to the Ministries of Agriculture, Rural Development, and Water Resources, the sum comes to slightly less than 1 percent of GDP, about the same as last year and one-third less than the 1 1/2 percent of GDP spent in 2020-21. In addition, most of the money is being spent on long-term programmes, while short-term measures to alleviate rural distress such as MNREGA and PM-Kisan are not showing any material increase, not even in nominal terms.

Finally, fiscal consolidation. It is, of course, commendable — as all the commentators have mentioned — that the government has used the bulk of the RBI dividend windfall to reduce the fiscal deficit. As a result, the government is now within striking distance of its objective of reducing the fiscal deficit to 4.5 percent of GDP in 2025-26.

But what about beyond next year? It is striking that several years after the pandemic has ended, the government has still not set out a medium-term fiscal strategy, nor even spelled out its longer-term fiscal objectives, beyond vaguely mentioning that it would like to keep reducing the debt ratio. Relatedly, the government still hasn’t seen fit to restore the FRBM Act, which was suspended during the pandemic.

There could be any number of reasons for this. For example, it could be waiting for the recommendations of the Sixteenth Finance Commission. But in the meantime the world is still waiting for the government to make a clear and solid commitment to longer-term fiscal prudence. And as a result, it will remain difficult to convince the ratings agencies to upgrade India’s bond rating.

So there we have it. You still want a score? Well, then, let’s say 10/10 for intentions. But as for execution, well, let’s just wait and see.

Nothing to See Here?

February 2, 2023

If you read the commentary on the budget, you’ll get the impression that it was not only solid, but stolid. That is, it didn’t contain anything interesting. The standard assessment runs like this: the government fulfilled its promise of reducing the deficit, using reasonable assumptions, and didn’t announce any new populist measures — or really any important measures at all. So, unless you are a fiscal nerd, nothing really to see here.

There’s only one problem. This impression is wrong. Well, not completely wrong. It is true that this was a prudent budget. But that doesn’t mean there wasn’t anything interesting in it. In fact, the budget contained three very significant measures. So significant that I’m tempted to call them radical. But that would be overstating it. So, let’s just say that they are definitely worth noting.

First is the remarkable capex push. The government is planning to increase capital expenditure by no less than 37 percent — on top of a 23 percent increase in FY 23. That’s an enormous increase in a very short span of time. Most economists are arguing that this is a great thing because, well, India needs more infrastructure. And so it does. But let’s think about the matter a little more deeply.

To begin with, what exactly is the government planning to do with all that capex money? Much of it is going to build roads, which is surely a good thing. But after that things get a bit fuzzy. The largest chunk — even more than on the roads — is going to be spent on the railways, possibly on things like the Ahmedabad-Mumbai bullet train and building some more spiffy stations, which are nice but not strictly necessary. And a significant sum will be spent on PSU telecoms (BSNL and MTNL), which arguably is not necessary at all.

All of which raises a question: will the returns on this investment actually exceed the cost of servicing the debt that is going to be incurred? Perhaps. I really hope so. But this is surely something to worry about, at a time when interest expenditures already exceed 3 1/2 percent of GDP, absorbing nearly half the centre’s revenues.

Even if this capex is truly worthwhile, one still has to wonder: what’s the rush? Why does the government feel that it needs to increase capex by nearly 70 percent in the short span of two years? (Yes, you doubters, 37 percent on top of 23 percent equals nearly 70 percent. Do the math.)

Presumably the answer here is that the government is trying to get the economy moving and isn’t sure that the private sector is going to do the job, so it plans to provide a big push by itself. The government’s diagnosis of the problem may well be right. Private sector investment does indeed appear sluggish. But it’s unclear whether the policy conclusion follows, that is whether public investment will actually spark self-sustaining rapid growth. Surely there must be some way to induce the private sector to start investing?

In the past, the government indeed had a strategy to do this: the PLI scheme of investment incentives. Indeed, in previous years, the PLI was the centrepiece of the government’s growth strategy, a highlight of the budget. But this year, it did not feature in the budget speech at all. This was the second most striking part of the budget announcements: the absence of the PLI. One wonders why.

The third significant aspect of the budget relates to centre-state fiscal relations. According to the revised estimates for FY23, gross tax revenues (GTR) increased this year by 12.3 percent, almost the same as the percentage increase in nominal GDP. But curiously, the states’ share of GTR increased by much less, only 5.7 percent. In other words, the lion’s share of the increase in gross tax revenues went to the centre, rather than the states. As a result, the centre was able to reduce its deficit.

What about next year? In FY24, the centre-state action is turning to the expenditure side. According to the budget, the government is planning to compress “other” current expenditure by an impressive 0.5 percent of GDP. It’s not clear (to me) where exactly this compression will fall, but this category contains current transfers to states, for example for NREGA. The centre says this reduction should be possible because it has adopted a new expenditure monitoring system (the Single Nodal Agency), which is yielding large efficiencies. Hopefully so. But the states may see this reduction in transfers differently.

By coincidence, the 0.5 percentage point reduction in other expenditure is exactly the same size as the reduction in the centre’s fiscal deficit. So, one could say that the centre is reducing its deficit by cutting transfers to states. If this is correct, there might not be any reduction in the consolidated fiscal deficit, as the reduction at the centre might be offset by higher deficits at the states. Of course, this is not inevitable. But it’s something to watch out for.

So there you have it. A major shift in the announced growth strategy from relying on the private sector (via the PLI) to focusing on government investment, coupled with a major shift in fiscal relations between the centre and the states.

We’ll have to wait and see how this strategy plays out. But one thing is already certain. Nothing to see here? Not a chance. There was quite a bit to see in this year’s budget.

India’s Big Chance

December 11, 2022

Let’s go back to India’s big chance, because it’s so….important. After all, as the retailers are constantly telling us, opportunities like this don’t come around every day. Of course, retail “opportunities” are not really serious chances. Urgent offers flood our e-mail in boxes every single day. But economic opportunities, well these are truly rare. They are also precious, because they hold out the hope of transforming the nation, lifting it up into the ranks of the advanced economies. So, we need to think about them very carefully.

There are some people who think that there is nothing to think about, because the process will be automatic. China’s slowdown will necessarily ordain the resurgence of India. After all, they argue, if global firms want to move out of China, where else would they go? There is only one country in the entire world that is even vaguely similar to China in terms of its population and economic potential. Add in the fact that New Delhi is actually offering incentives for firms to shift, and India’s future as the workshop of the world seems inevitable.

Without doubt, this argument seems compelling. Yet it is fundamentally flawed. As Arvind Subramanian and I discuss in our recent piece for Foreign Affairs, most global firms are not really looking for a-country-that-seems-similar-to-China. They have other criteria. They want to reduce their risks, and they want to preserve access to their supply chains.

On those criteria, India right now is not an ideal match. Perceived investment risk–the risk, say, that a seemingly attractive policy framework will later be changed in a way that would render the firm’s investment unprofitable–is quite high. This is why even domestic firms are reluctant to invest. In addition, protectionist barriers are high and rising. Between 2014 and 2021, there have been some 3,200 tariff increases, affecting about 70 percent of total imports.

So, global firms are thinking long and hard about alternatives. A long time ago, way back in the 1980s and 1990s, before firms started to invest in China in a big way, the preferred destination was Southeast Asia. There are still legacies of that investment boom, global factories littered all across ASEAN: for cars in Thailand, electronics in Malaysia, sneakers in Indonesia, clothing in Vietnam. It would be straightforward to revitalize and expand this industrial base.

In addition, ASEAN countries meet global firms’ two main criteria: they have welcoming, stable economic frameworks and they are very open. Vietnam, for example, has negotiated no less than 10 free trade agreements since 2010, with major economies such as China, the EU, the UK, and its regional ASEAN partners.

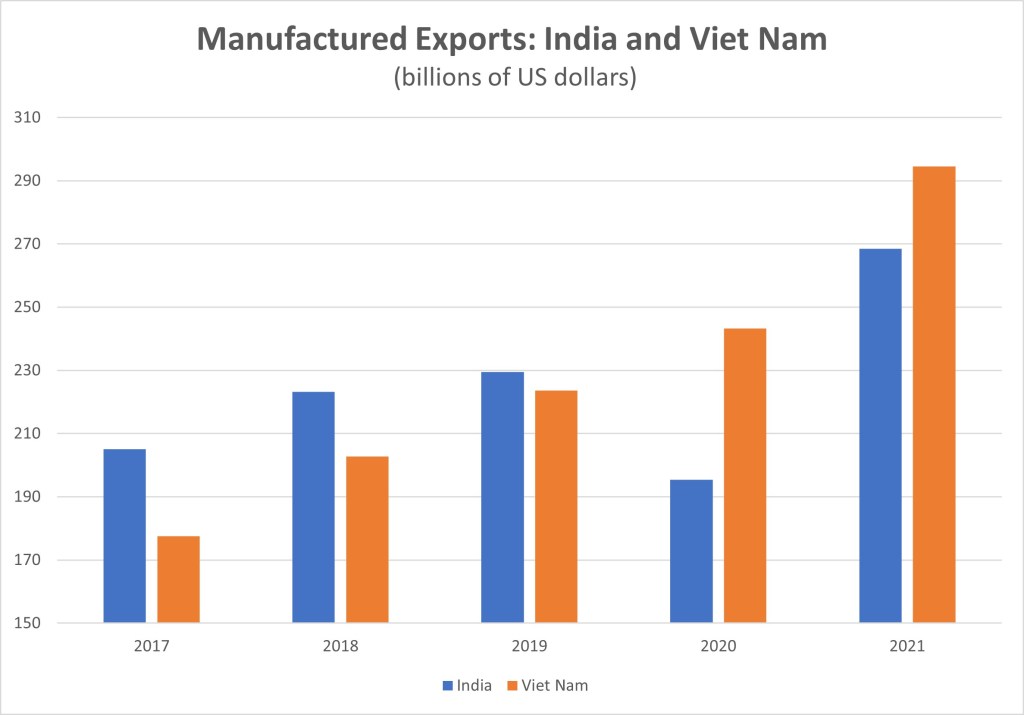

As a result, investment has already begun to shift to Southeast Asia. And the results are already beginning to show. Just a few years ago, India’s manufacturing exports far exceeded those of Vietnam. But thanks to foreign investment the reverse is now true.

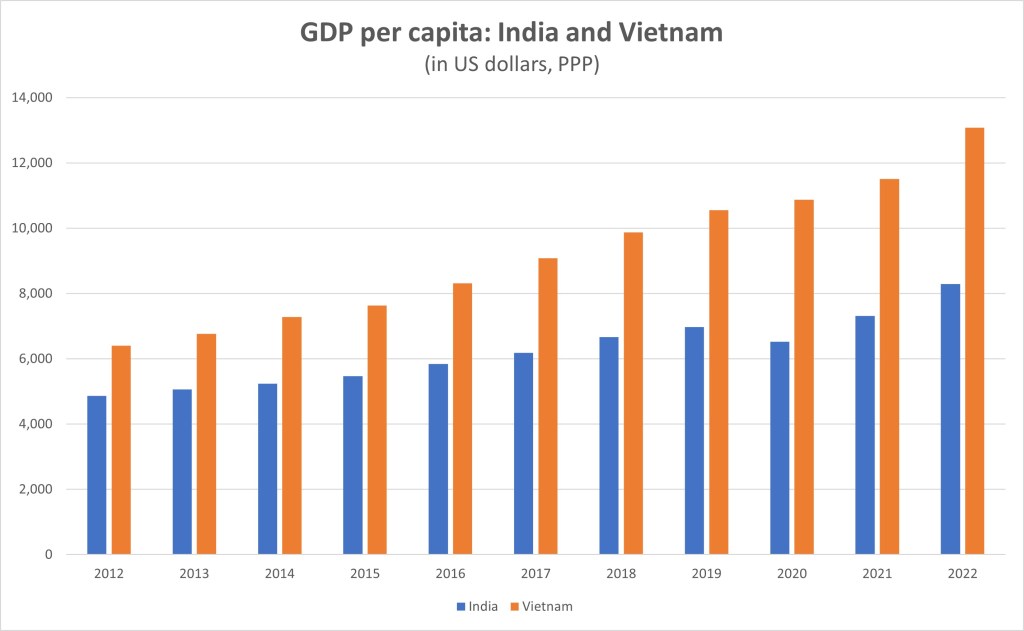

As a result, Vietnam’s per capita income has also soared past India’s.

Of course, the game is far from over. There will surely be much more investment that will be redirected out of China in the coming few years, and much of that could indeed come to India. Apple’s plans to expand production in India shows the potential. But for India to seize this opportunity with both hands, subsidies will not be enough. The economic environment needs to become much more predictable and open.

How can this be done? Arvind Subramanian and I set out an agenda in an earlier piece for Foreign Affairs.

And for those who prefer videos, here’s my interview with the BBC.

Happy Independence Day!

August 15, 2022

On this Independence Day, it’s good to realize that India is facing an historic opportunity: the country has a real chance to become a exporting powerhouse.

Some people have argued that there’s no point in trying to push exports right now, since the West is headed for recession. But this ignores the possibility of gaining market share. In fact, the stars are aligning for India to do so, as Arvind Subramanian and I explain in our latest article for Project Syndicate. Over the past decade, the shocks that have transformed the global trading system have all disfavored China and helped India. The Global Financial Crisis shrunk trade in goods, but not services; Covid shifted service activities offsite; and Russia’s war is encouraging “friend shoring”. All this has opened up a large opportunity for India.

So, on this Independence Day, sure, let’s think about the accomplishments of the past. But we should also think about the future. There is a glorious future out there, tantalizingly within reach. India just needs to go out and seize it.

Happy Independence Day!

Have We Seen This Movie Before?

May 20, 2022

It’s the weekend. Time to relax and catch a movie. So you settle into the couch and turn on the tv, looking for a nice film to stream. But right away you run into a problem. There are way too many titles to choose, and no one has any idea which one to watch. Finally, someone suggests Ek Duuje Ke Liye.

Hmmm. It is true that you haven’t seen it. But on the other hand it’s a really old movie, and you’re really not sure how it would stand up today. Yet again, it is a classic; your parents love it and you do know and like the songs. So you give it a try.

It turns out to be a good choice: the songs and the plot grab you. But just when you really start to get into the film and things are really getting tense, someone blurts out, “This is going to end badly. Very badly.”

“How do you know?”

“Because I’ve seen this movie before.”

“Wait…! I thought you said you hadn’t seen this film before!”

“I haven’t.”

“Huh?”

“I mean I haven’t seen Ek Duuje Ke Liye. But I recognize the plot. It’s exactly the same as Maro Charitra, which I have seen. And I assure you, it ends very badly.””

” Oh.”

What does this have to do with India’s economy? Everything.

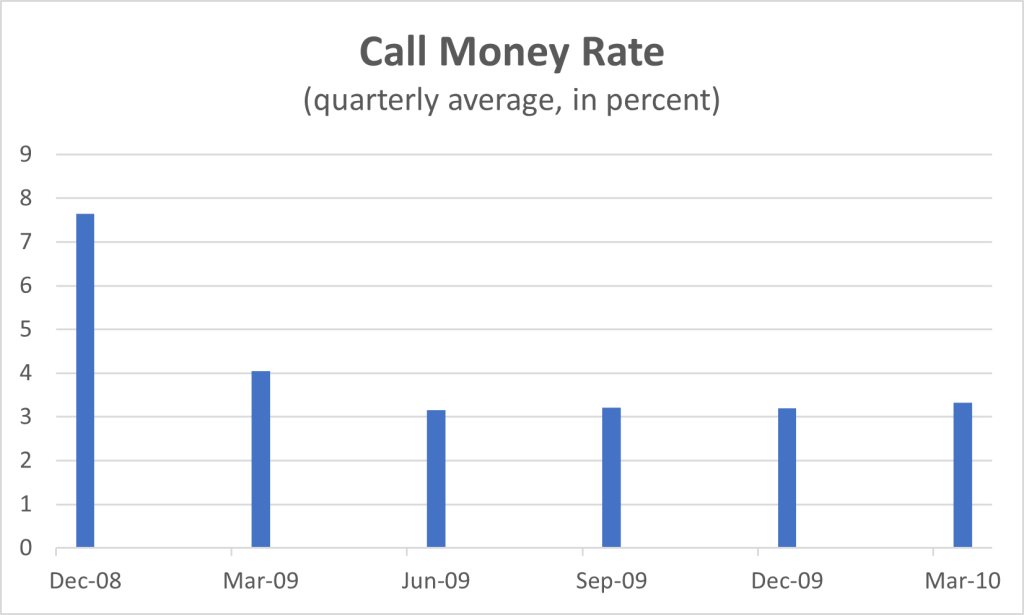

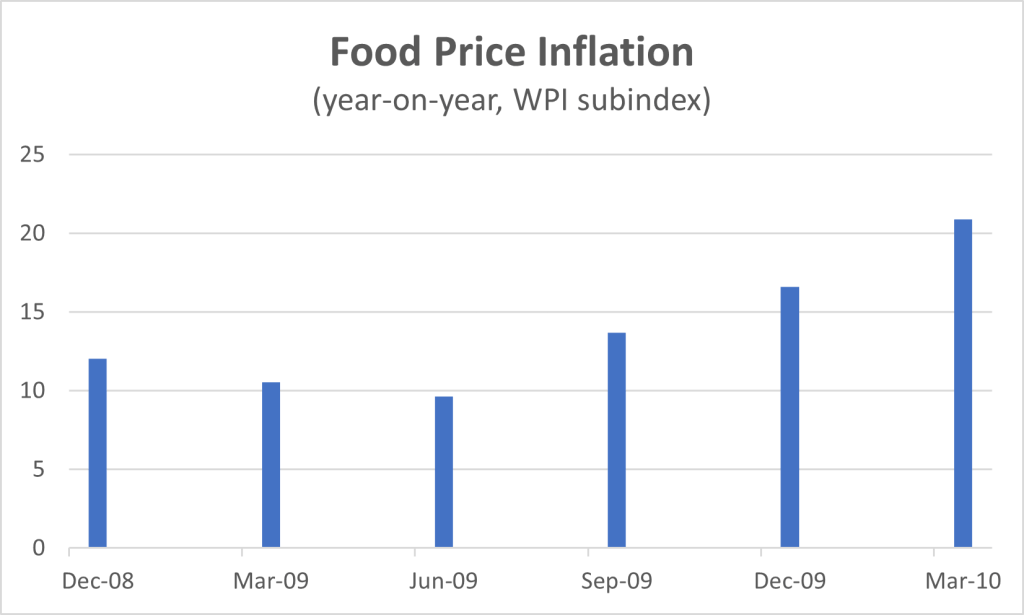

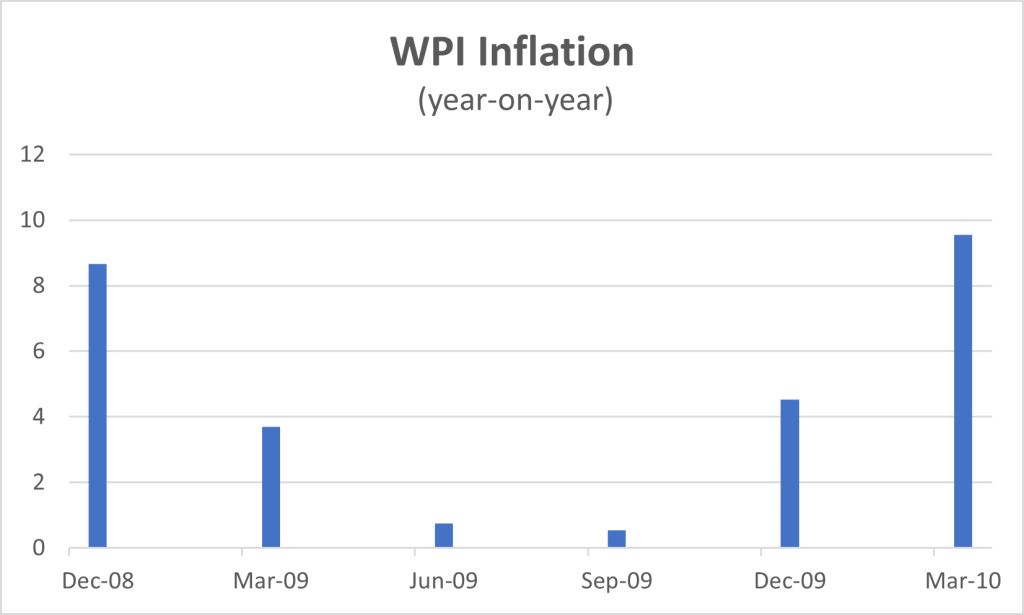

Cast your mind back to 2009. Back then, India’s economy was struggling to recover from the blow inflicted by the Global Financial Crisis. So, the nation’s lonely eyes turned to the RBI, in the hope that the central bank could breathe some life into the feeble economy.

The RBI responded with alacrity and decisiveness. It quickly cut interest rates to levels that had hardly been seen before. Within 6 months, call money rates were reduced by an astonishing 450 basis points compared to their December 2008 levels, bringing them down to just 3.2 percent.

At the time, no one worried about inflation. Sure, it was known that food prices were increasing extraordinarily rapidly — by double digits, in fact. But most people argued that the RBI couldn’t do anything about food prices, and that there was no need to worry that food inflation would feed into other prices, because the economy was so weak. After all, how could firms raise prices when demand was so low?

It seemed like a good argument at the time. And for a while it actually seemed to be true. Even as the RBI was cutting rates, WPI inflation — which was the central bank’s target at the time — was falling. By June 2009, WPI inflation had almost completely disappeared.

But then something went wrong. In December, inflation started to rebound; by March 2010 it had soared to nearly 10 percent. It turned out that, contrary to expectation, food inflation was indeed feeding through into other prices. (See the previous blogpost for a discussion of that episode.)

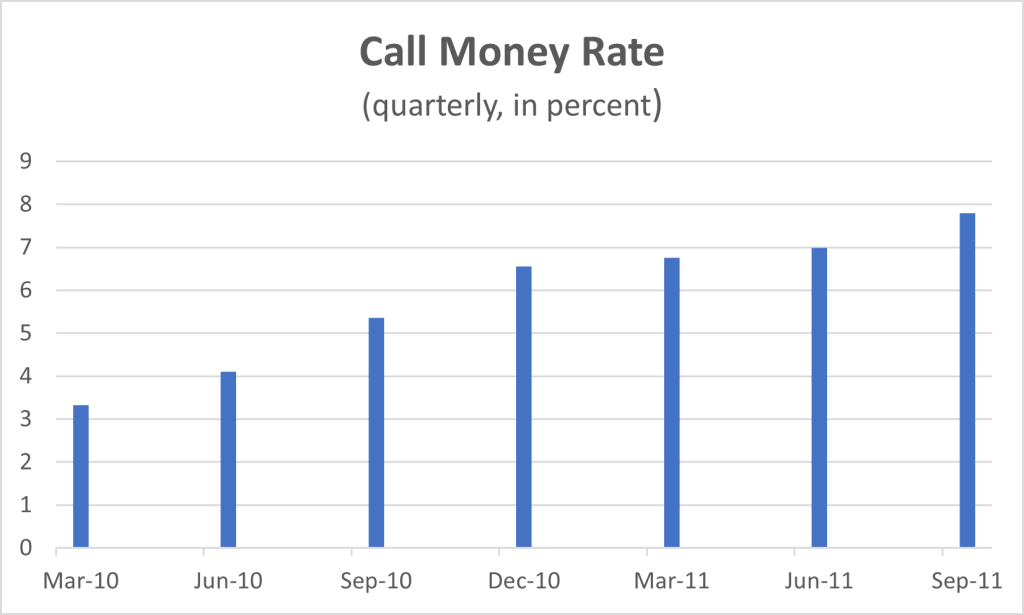

At that point, the RBI was caught. It really, really, really didn’t want to raise interest rates, because that would endanger the nascent recovery. Moreover, in the context of the then-prevailing paradigm, raising interest rates didn’t even seem necessary. Surely, the price rises were due to some exceptional circumstances, and would subside as things went back to normal.

So, the RBI proceeded cautiously, raising interest rates gradually and in modest increments. It took the central bank one and a half years to increase the call money rate back to the December 2008 level. In other words, the central bank was very quick to cut rates when the economy flagged but very slow to normalise rates when inflation materialised.

How did this strategy work out? Ummm. Not so well. After the RBI “fell behind the curve” with its interest rate increases, prices skyrocketed at a double-digit pace for the next two years. It took four full years before the central bank managed to get inflation back under 6 percent on a sustained basis. And in the meantime, the loss of macro stability caused an exchange rate crisis in 2013, forcing the RBI to increase the call money rate to around 9 percent, amongst other extraordinary actions.

When some semblance of stability was finally restored, the new government vowed to make sure that this would never happen again, bringing in an Inflation Targeting regime, which made the RBI commit to aim at keeping inflation to 4 percent, with at most a 2 percent deviation from this objective. To show that it was serious, the government enshrined this regime in law.

Fast forward to 2022. Food prices are once again soaring, and this has again caused a surge in inflation. And just like before, some economists are arguing that high inflation can’t really persist since the recovery is so weak. (See the previous post.)

There are some differences between the current and earlier episodes. In particular, this time the government has prudently eschewed a large fiscal stimulus. But even if the demand pressure is lower this time, the supply pressure is higher. Russia’s invasion of Ukraine has endangered 28 percent of the globally traded supply of wheat, 29 percent of barley, 15 percent of maize and 75 percent of sunflower oil. China’s repeated lockdowns have caused industrial production to fall in the “workshop of the world”. Meanwhile, the US is having difficult increasing its supply, because it is having enormous difficulties convincing people to return to offices — and even to the workforce — after two years of pandemic. And then there are the problems in the oil market.

As a result, global supply just cannot keep up with demand, causing inflation to soar all over the world. Inflation in the EU and US has climbed to 8 percent. Inflation in the UK has hit 9 percent, with the Bank of England forecasting that it will reach double digits.

In these circumstances, one might have expected the RBI to be emphasizing that it has learned the lessons of 2009. These lessons are three:

- Broad-based and sustained increases in food prices are dangerous, as they can set off a serious inflation fire.

- Food prices increases are particularly dangerous when interest rates are at exceptionally low levels, as this only fans the inflation flames.

- In such circumstances, the RBI cannot sit on its hands. It needs to act quickly to douse the flames, by raising interest rates as fast as possible to normal levels and beyond.

How can the RBI reassure the public that it has indeed learned these lessons? Not with a panicky, poorly explained rate increase. Rather, by providing a convincing assessment of the inflation outlook and risks; a detailed description of its strategy; and an explanation of why it is convinced this strategy would be sufficient to bring inflation back to 4 percent in a timely fashion.

But what do we see in the Monetary Policy Committee (MPC) minutes that were released this week? Deputy Governor Patra, the person in charge of the institutional memory of the RBI, did indeed compare this episode to a previous one. But he mentioned 1993-94, a period where nothing momentous happened in India. No one on the MPC mentioned the previous episode of high inflation at all.

In fact, the minutes contain very little discussion of the outlook. Even when the MPC raised interest rates in its emergency May 4th meeting, it didn’t provide a new set of inflation projections to justify its actions. So, we still don’t know the RBI’s assessment of the size of the problem. Nor do we have a clear idea of its strategy to deal with it.

What exactly, then, do the minutes contain? Well, all the members do clearly acknowledge that there is some sort of problem. But instead of focusing on finding a way forward, much of the discussion apparently focused on assigning blame. Deputy Governor Patra pointed to the US Fed’s tightening of monetary policy, worrying that as other central banks follow the Fed this could “render the economy stillborn”. Ashima Goyal complained that the government’s failure to cut fuel taxes is “raising inflation”. Jayant Varma complained that his colleagues lacked urgency.

So, perhaps we have indeed seen this movie before. Well, at least it had some good songs.

Dangerous Curve Ahead!

May 17, 2022

The recent spurt in inflation has set off alarm bells across the nation. The Times of India has fretted that we are now living in Pricey Times, where inflation is putting pressure on household budgets. And the Indian Express has no doubt whom to blame for this situation, complaining in an editorial that the RBI has “been underestimating the price pressures in the economy and has fallen behind the curve when it comes to managing inflation.”

But not everyone agrees with this assertion. On Sunday, a member of the Monetary Policy Committee, Ashima Goyal, fired back, stating firmly that the RBI is most definitely “not behind the curve” (i.e., too slow) in raising interest rates.

What fun! Everyone loves a good debate. So, let’s dive in and see what this is all about.

Professor Goyal makes three points. First, inflation has surged because Russia’s invasion of Ukraine has reduced global supplies of oil and food, causing their prices to soar. In other words, it’s foreigners who are to blame for the inflation. Not the RBI.

Second, the RBI should essentially ignore the global supply problems. After all, the central bank can’t do anything about the world price of oil. Moreover, prices of commodities are cyclical; they will go down as quickly as they went up. And when they do start to fall, inflation will subside — even if the RBI does nothing.

Third and consequently, interest rate policy should be geared instead to developments in domestic demand. Rates should be set at high levels only when growth is strong and demand is too high. Since right now growth is weak, interest rates need to be maintained at low levels.

It follows that the RBI policy stance is — and has been — completely appropriate. The real problem lies with those who are complaining that the RBI is behind the curve, for if their recommendations are followed, the result would be disaster. An aggressive increase in interest rates would have only a small effect on inflation. But it would have a big effect on output: the nascent recovery would be derailed.

Well, well. That is quite a spirited defence! But is it correct? We cannot settle this matter in one go, as that would result in a blogpost that is far too long.

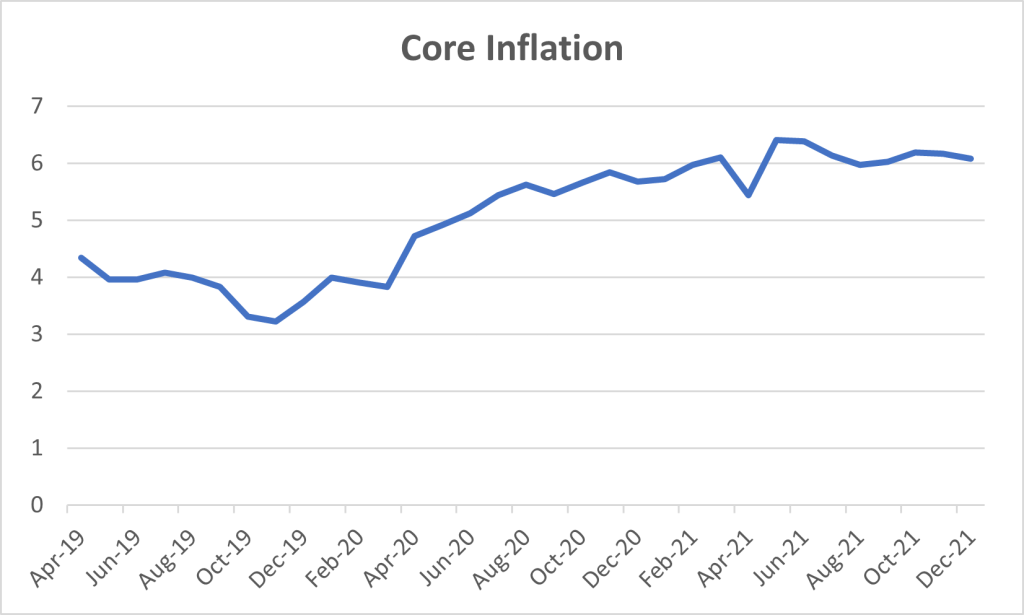

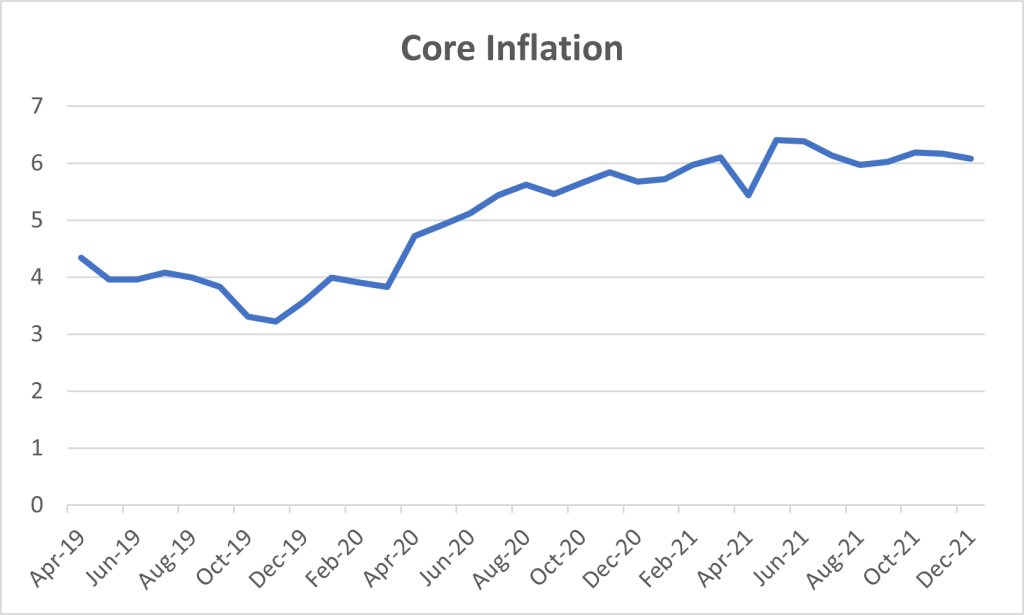

But let’s go through a first round. Start with the claim that inflation was firmly under control before Russia decided to start a war. To assess this assertion, let’s use the same measure of underlying trends that the RBI uses, namely core inflation, which strips out from the CPI items whose prices are volatile, like food and fuel.

So, what was was happening to core inflation before the war started in February? Here’s the graph.

You can see that in 2019 core was running at the target rate of 4 percent. But over the subsequent two years it just rose and rose until it reached 6 percent. So, no, inflation was not firmly under control before the war. It was some 200 basis points higher than it should have been.

What about the second point, that the RBI should ignore developments in oil and food prices? Sure, it’s true that the RBI can’t do much about global prices. But that doesn’t mean it should ignore them. In fact, ignoring them would be dangerous, very dangerous indeed.

The reason is that the increase in commodity prices could easily spill over into other prices, pushing overall inflation even beyond 8 percent.

Consider first the potential impact of the oil price increase. The soaring cost of oil has caused a large loss in income for India, since the country will have to pay an extra 1 percent of GDP this year for the oil imports that it needs. (See the post of March 2, 2022 for a more detailed explanation.)

Who is going to pay this 1 percent of GDP? Obviously, no one really wants to do so. So, firms are responding to the increase in their costs by increasing their prices. And soon workers will be responding to these price increases by trying to get wage increases. In other words, firms and workers are going to be playing a game of “pass the parcel”, in an attempt to shift the burden of the income loss from one to the other. But the income loss is there. So, someone has to bear it. That means there needs to be a party that intervenes and calls a halt to this game, before a wage-price spiral drives inflation into double digits. That party is the RBI.

But wait, I hear you say. India is not a Western country. There are no large unions, which will go on strike for wage increases when prices go up. True enough. But there is indeed an Indian equivalent, which is even more automatic. It’s called Dearness Allowance.

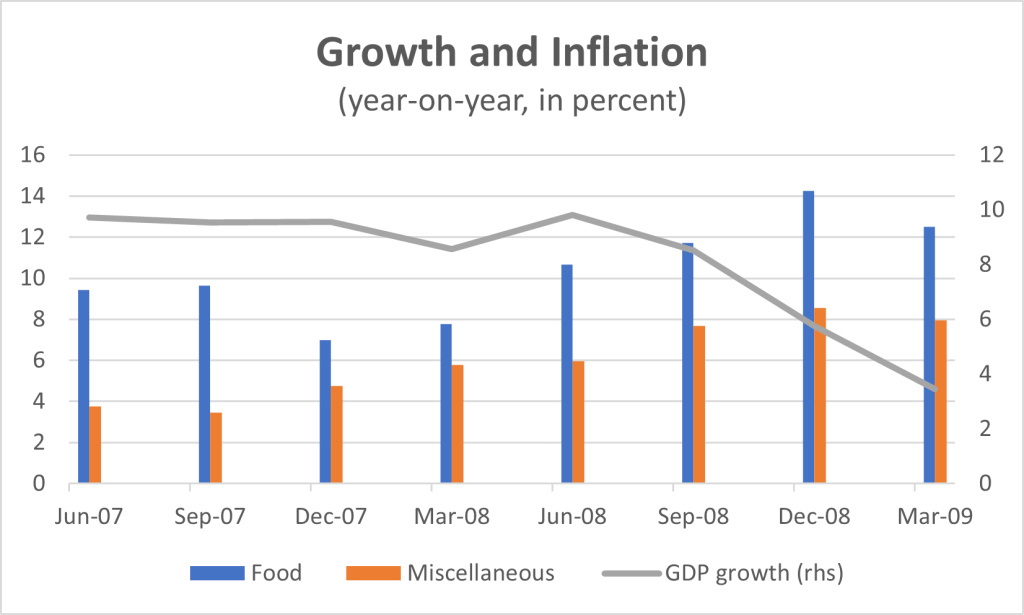

More to the point, there is a large service sector, a very large service sector. And we know from past experience what happens when there is a large increase in food and fuel prices: service firms respond by increasing their prices to compensate. You can see this by considering what happened during the previous period of high inflation.

During that period, in the mid-2000s, inflation behaved completely differently from Professor Goyal’s model. When India was booming, inflation was actually quite moderate. Then, after the Global Financial Crisis, growth slowed sharply but inflation rose.

Why did this happen? You can see the answer in the chart below. During the boom period, service price inflation (orange bar, as proxied by the “miscellaneous” category) was running at less than 4 percent. But when food prices started to increase at a double-digit pace, the prices of services started to accelerate, as providers (think about beauty salons) started to increase prices so as to maintain the living standards of their workers. After all, people need to eat.

By December 2008, service inflation was running at 8 percent, pushing overall inflation into double digits.

So now we get to Professor Goyal’s third point. Should interest rates be raised? Indeed they should. Underlying inflation has been running far above the RBI’s 4 percent target for nearly two years now. And now the large spike in commodity prices runs the risk of triggering a wage-price spiral that could send inflation even higher.

We know from the experience of 2013-15 that once inflation becomes entrenched, it becomes very difficult and painful to eradicate. That means that the RBI needs to act nimbly, taking action whenever inflation pressures are emerging on the horizon.

By this standard, it’s already late; the RBI should have raised rates months ago.

The RBI is behind the curve.

The Long and Winding Road

May 13, 2022

Have you ever decided to a hike to a temple? Then you know how it goes. You can’t really see where you are going, since the trail winds this way and that. So you just walk and walk and walk, going up and up and up, wondering at each turn whether you are getting close to your destination.

The trail seems to go on forever but finally you arrive, at which point you are engulfed by a wonderful feeling of satisfaction. Sure, it took a great deal of time and even more effort to get to the temple, but now you get to enjoy the rewards. You ring the bell to let the deity know you’ve arrived. You look around and enjoy the wonderful view, maybe even have something to eat. And then you rest.

For a while, life seems perfect…until you realise that it’s getting late, you have to get back home, and you have a long road ahead. So, you pick up your weary bones, pack up your picnic lunch, and set off on the trail again. But there’s a problem. It turns out that there are actually many paths to choose, and you’re not sure which is the right one. One of them leads you home. But the others lead…who knows where? And did I mention that it is getting late?

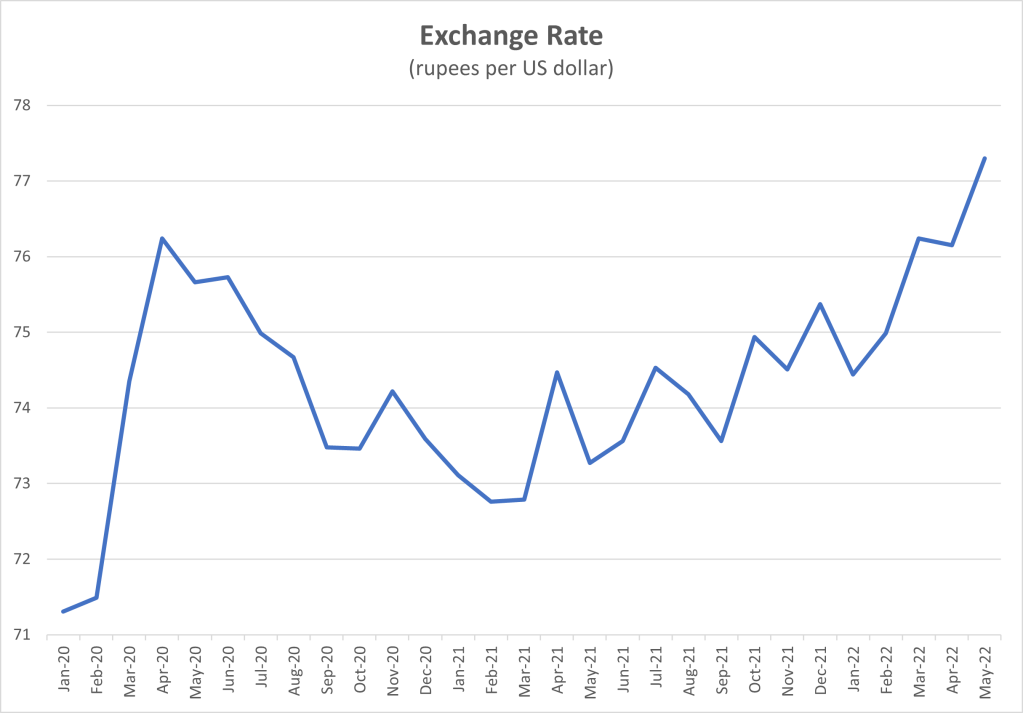

This is precisely the problem the RBI is now facing. For the past few years, life has been good for the central bank. Foreign exchange reserves just kept going up and up, the exchange rate was fairly stable, while inflation seemed to be under control. So, the RBI felt free to cut interest rates. And cut. And cut. And cut.

At each step of the way, the RBI was flooded with praise. The government was pleased that government bond rates were falling, as this reduced the cost of financing their enormous budget deficits. Businesses were happy that the cost of imports was stable, while low interest rates helped improve their profits. And others were happy that the RBI was stimulating demand, to help the economy recover from the pandemic. So, yes, life was good for the RBI. Very good.

Of course, some people like Rajeswari Sengupta did warn as early as 2020 that the RBI’s lax monetary policy was running the risk of reigniting inflation. But those people were merely pesky economists, who could safely be ignored.

OK. Let’s rephrase that. Pesky economists could certainly be ignored. But safely? Well….

Fast forward to May 2022. Inflation has taken off and is now nearly 8 percent, double the 4 percent target. The exchange rate is slipping and sliding, falling to Rs 77.3 per dollar last week, an historically low level. Consequently, the RBI has been forced to increase its repo rate, causing g-sec rates to jump to 7.3 percent. Not to put too fine a point on it, but this situation has not exactly been met with the same degree of praise the RBI had previously enjoyed. See for example this comment from the Ministry of Finance.

We discussed in the previous post (April 13, 2022) how the country wound up in this situation. TL; DR: no, Russia’s invasion of Ukraine was not the cause of the problem; it was only the final blow.

So, let’s now focus on the RBI’s dilemma. The RBI seems to have three objectives: inflation, the exchange rate, and the g-sec rate. To achieve these objectives, it has a three-pronged strategy:

- raise the repo rate to control inflation

- sell foreign exchange reserves to stabilise the rupee exchange rate and

- purchase government bonds in the open market to control g-sec interest rates.

Sounds good, right? Three objectives, three instruments. No problem!

But there is a problem. The three instruments are not actually independent. Use one instrument and you destabilize the others. Let’s consider one example: liquidity.

During the years of lax monetary policy, a tremendous amount of liquidity accumulated in the banking system. The RBI now needs to wind back this liquidity, as it needs tight monetary conditions in order to bring inflation back down. But the clash amongst the instruments is making it impossible for the RBI to control liquidity. Consider:

- On May 4, the RBI increased the CRR — the amount of cash that commercial banks need to deposit at the central bank — in order to reduce liquidity.

- But when the RBI purchases government bonds in the market, to keep a lid on g-sec rates, it pays banks in cash, thereby…increasing liquidity.

- Then again, when it sells dollars in order to prevent the rupee from depreciating, the banks have to pay for the dollars with rupee cash, thereby reducing their liquidity.

Up. Down. Round and round. The RBI’s three-pronged strategy is making it impossible to control liquidity.

This may seem a very specific example. But the problem it illustrates is actually quite general. In fact, there’s even a name for it: the trilemma. According to the trilemma, the RBI’s pursuit of three objectives is ultimately impossible. For short periods, a central bank may seem to control inflation, interest rates, and the exchange rate at the same time. But ultimately such a strategy is incoherent, and bound to fail.

To understand why, consider the plight of a foreign portfolio investor (FPI) in government securities. The FPI knows that the RBI is trying to cap g-sec interest rates, control the exchange rate and reduce inflation. All these objectives are worthy in the eyes of an FPI. Indeed, if the strategy succeeds, the FPI will make a lot of money. But what if it fails? After all, the FPI knows the goals are inconsistent, and the RBI will have to give up on at least one of these objectives. So, it doesn’t know how far the RBI will go in any of these directions.

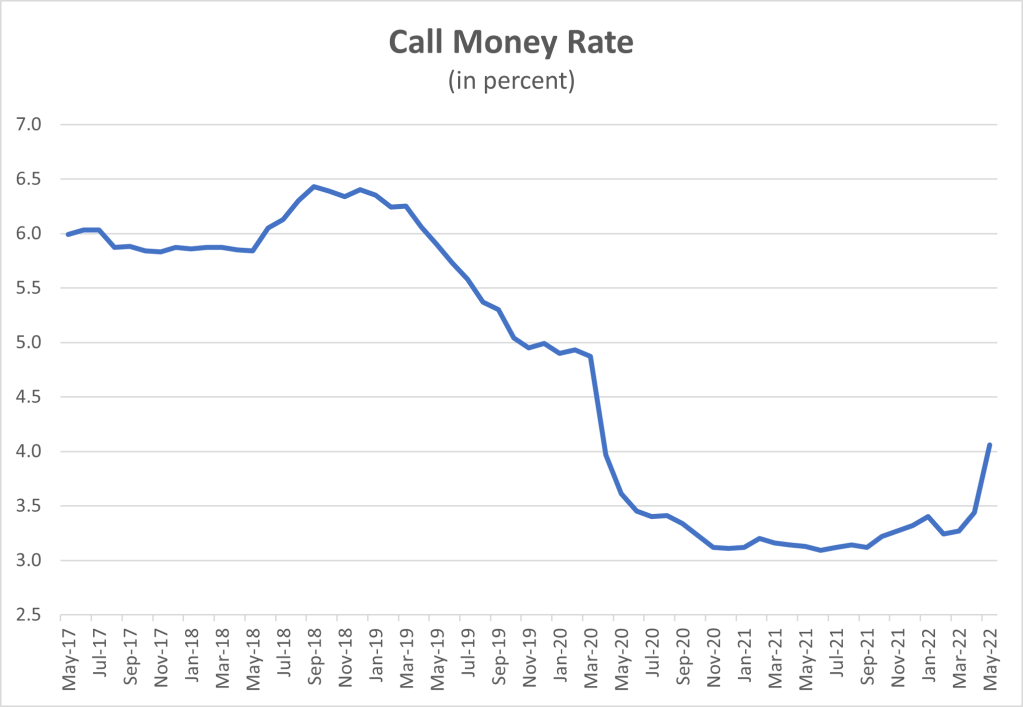

In particular, it doesn’t know how far the RBI will be willing to raise short-term rates to reduce inflation. We’ll examine this issue in more detail in a future post, but for the moment let’s assume that in order to bring inflation back to the 4 percent target, the RBI needs to increase short-term rates back to where they were in 2017, when inflation was safely under control.

The following chart shows developments in the weighted average call money rate. This is the rate that banks use for transactions amongst themselves — it’s a much better indicator of what is really going on with monetary policy than the constantly shifting policy rate (the repo rate, the reverse repo, the VRR, the standing deposit facility…). The chart shows that even after the May 4 emergency announcement, short-term rates are still some 200 basis points below their 2017 level of 6 percent.

So, the FPI thinks as follows. There’s a chance the RBI could raise short-term rates by 200 basis points in which case it would have to abandon its cap on g-sec rates, leading them to rise considerably. In that case, g-sec prices would collapse and the FPI would suffer large losses. But since the RBI’s strategy is inconsistent, there’s no way to calculate the risk of a major loss. And in the face of such uncertainty, there’s only one thing for the FPI to do: get out of the market.

Moreover, now is a good time to get out of the market, since the RBI’s interventions are keeping g-sec prices high and the exchange rate stable. In effect, the RBI is offering a subsidy for any FPI that wishes to exit, a subsidy that might be withdrawn at any moment. So, the FPI decides to close its position, selling its g-secs and converting the proceeds into dollars.

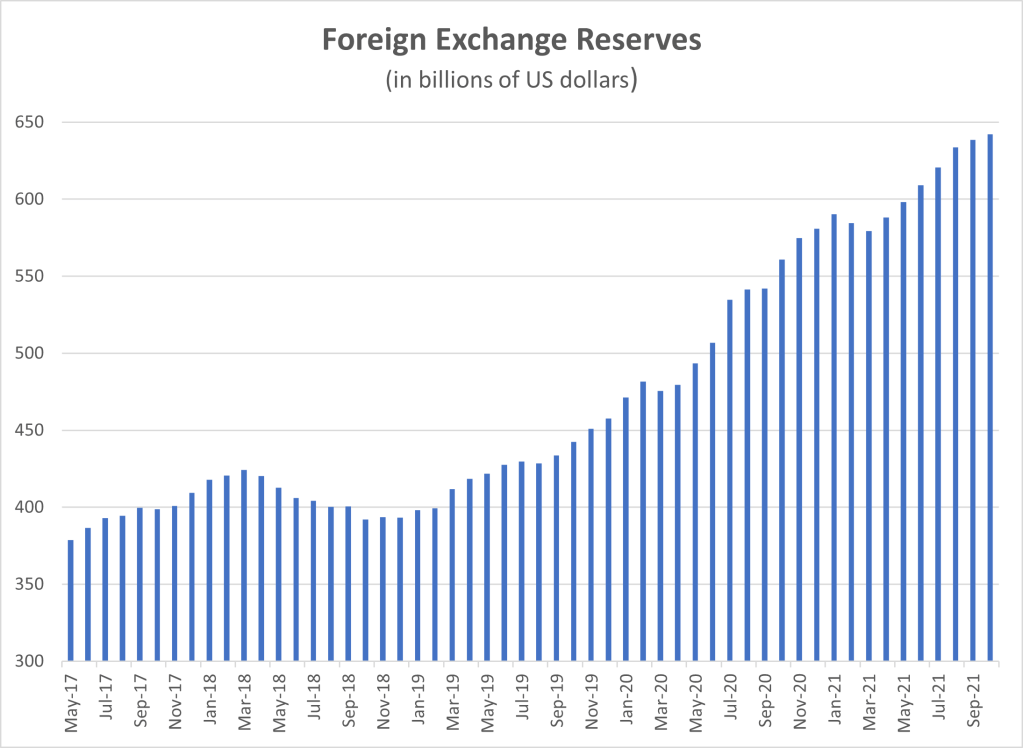

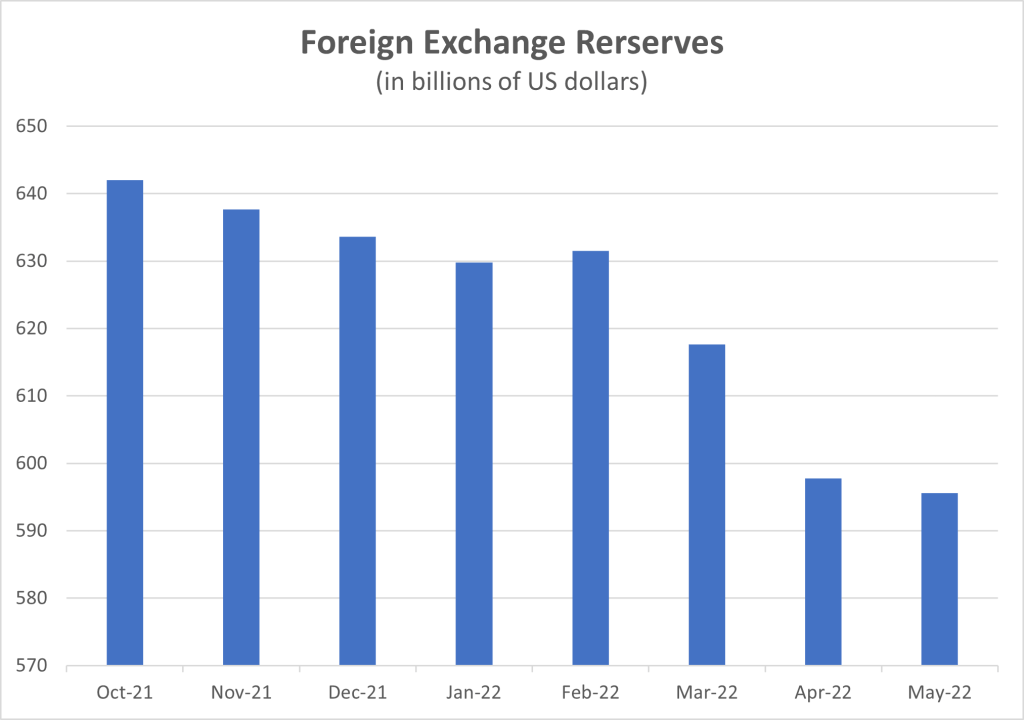

In this way, the policy inconsistency creates a vicious circle: the inconsistency makes markets nervous, and market nervousness creates selling pressure that causes the policy strategy to collapse. Since October 2021, the RBI has lost some $46 billion in reserves, trying to stabilize the rupee in the face of large capital outflows. It still has some $596 billion left in its foreign exchange kitty, but even so the pace of the decline is alarming, particularly over the past few months.

On the domestic side, if investors are worried that the RBI won’t be able to cap g-sec rates forever, they will be reluctant to buy g-secs at the current rate in the auctions. But then how will the government finance its large deficit?

So, let’s sum up. For the past two years, the RBI has been sitting tranquilly on top of a mountain. But now the central bank needs to get back home. For the moment, it is looking this way and that, trying to decide which path it is going to take. Indeed, it seems to be trying to go down three different paths all at once, a “strategy” that is only damaging the central bank’s credibility and risking another “mini-crisis”, as occurred in 2013.

In the end, there is really only one path home, only one path that leads to the target enshrined in the law of the land. The RBI needs to focus on controlling inflation, and to follow this path until the end, when inflation is securely back at 4 percent.

It’s going to be a long and winding road. But the sooner the RBI sets off, the sooner it will get there. And the calmer the nation will be.

As we wait, it might help to chant a mantra. Perhaps this one.

Snake Eyes

April 13, 2022

Some people just love to gamble. They have a vision, and believe in it so strongly that they put all their mental and financial resources into realizing their goal. In some ways, you can only admire their daring and determination. That is, until things go wrong.

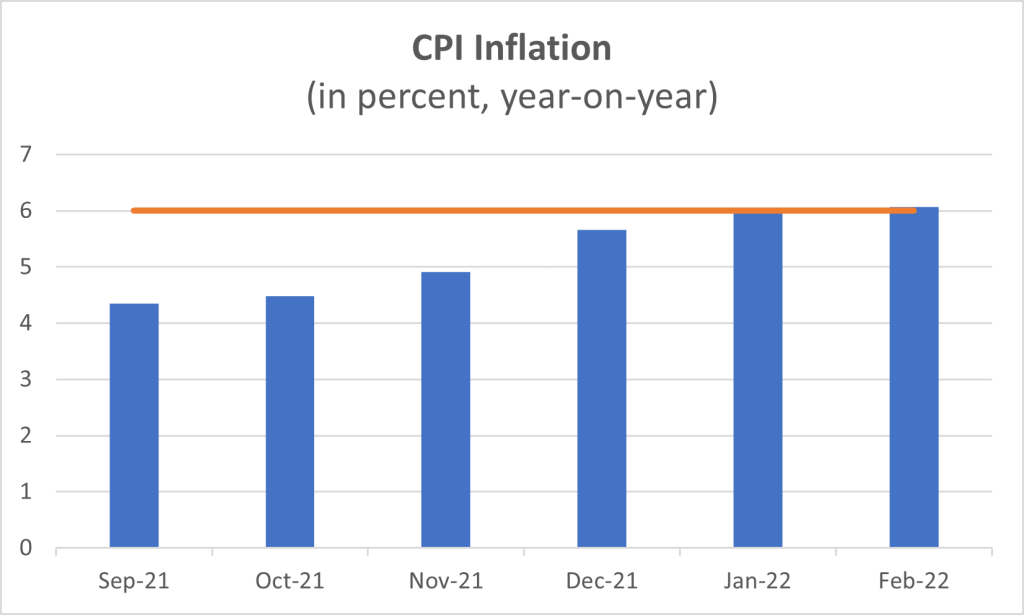

Consider monetary policy. Starting in October, inflation began rising toward the RBI’s legally mandated upper bound of 6 percent. By January, inflation had actually reached the upper bound.

Even then, the RBI remained unfazed, insisting the trend was merely temporary and inflation would soon recede toward its central target of 4 percent. So there was no need to tighten the “accommodative” monetary policy. Not now. Not in the future.

In making this assessment, the RBI was effectively placing a double bet. First, it was betting that the “imported” inflation coming from overseas would be temporary. And second, it was betting that these pressures could be bottled up at the wholesale level, and not pass through to retail prices.

Why did they make such a bet? Start with imported inflation. The RBI knew, of course, that inflation in the US had been rising for even longer than in India. But it agreed with the US Federal Reserve that the problems were temporary and would surely fade once the pandemic eased, allowing global supply chains to be restored. Even when Russia invaded Ukraine, adding to the problems by disrupting supplies of fuel and food, there was still some hope that the war might end quickly and normal trade could soon resume. So, perhaps if the RBI proved patient, the imported inflation would just go away.

The RBI also had its second line of defense. That is, even the first bet proved wrong and imported inflation did continue, it might not be passed through onto domestic prices. After all, domestic demand was soft, meaning that firms would be reluctant to increase their prices by as much as their increase in costs, for fear of losing sales. And this was not just some theory: the corporate data did indeed show that firms were reducing their margins.

Moreover, much of the increase in the WPI was being driven by two items, fuel and food, whose wholesale prices were linked to global developments, but whose retail prices could be influenced by government action. The government was not allowing pump prices to increase even as global prices were soaring. And it was providing subsidised food to consumers, not just through the regular Public Distribution System (PDS), but through the PGKY, the special free food grain scheme. These two policies acted as national barriers against the global tide.

So, the RBI did have its reasons to think that CPI inflation might soon subside. Even so, it was a big bet, since WPI inflation was running at more than 13 percent.

And now we know the bet failed. It’s not just that March inflation clocked in at nearly 7 percent. In a way, that is the least of the RBI’s problems. The real problem is that the entire premise underlying the RBI’s bet has proved wrong.

Consider the first element, global inflation. The Fed has now acknowledged that the global supply problems will not be resolved any time soon. After all, the disruptions from China are not ending; they are expanding. Of China’s 100 largest cities (measured by GDP) all but 13 are now under some form of lockdown, with Shanghai now under a total lockdown, confining 25 million people to their homes for the first time since the pandemic started. Meanwhile, Russia’s war has turned out not to be a short-lived affair; it is now deep into its second month, with no end in sight, ensuring that commodity prices will remain high for a long, long time. As a result of these disruptions, inflation in Europe has climbed to 7 1/2 percent while US inflation has reached 8 1/2 percent.

At the same time, the barriers that the RBI had been counting up to hold back this global tide have toppled. Every single one. The cost pressure on firms has been so intense that they have had to effect large price increases. The pressure on the budget has been so severe that the government has been forced to increase pump prices. And the supply management efforts have proved no match for soaring global food prices.

So, where are we headed? Nowhere good. Just consider that the acceleration in the CPI in March had nothing to do with fuel prices. This inflationary impulse is still to come. It will start in April, when the index will reflect the increase in pump prices; it will then followed by increases in the price of all the goods that need to be transported; and then — who knows? — there could be a wage-price spiral as workers and firms try to recoup the increase in their costs.

That’s not all. For much of the past fiscal year, CPI inflation has been held down by exceptionally low food inflation, even as prices at the wholesale level have been rising rapidly. But this luck has now ended. In March, the wholesale increases started to be passed through in a major way — a key reason why consumer prices increased so sharply.

With food constituting half of the CPI basket, and with further large WPI increases in the pipeline (see chart below), well….you can do the math. But maybe you shouldn’t; it’s just too grim.

Chicago Wheat Futures (in cents per bushel)

So, there we have it. The RBI has rolled the dice, and it has come up snake eyes. Global inflation is not only continuing; it is intensifying. And the consequent wholesale price increases are being passed through into consumer prices.

How will the Reserve Bank respond? Will it continue to be daring, and roll the dice again? Or will it decide that the time for gambling is over?

Stay tuned. It’s going to be interesting.

Get the Balance Right

March 9, 2022

With every passing day, it becomes more and more apparent that high oil prices — very high oil prices — are going to be with us for some time. So, let’s go back to the dilemmas that this shock is going to pose. Recall from the previous post that the increase in oil prices acts just like a tax on the country, reducing India’s national income. So India, just like any household faced with a loss of income, can respond in one of two ways. It can reduce spending or it can borrow and run down assets. In other words it has two choices: adjustment or financing.

There’s no one “correct” solution to this dilemma. The artistry, then, lies not in figuring out whether adjustment or financing is the best option to follow. It’s all about getting the balance right.

At the broadest level, the oil shock is going to have three nasty effects. It will:

- Reduce growth

- Increase inflation

- Widen the current account deficit

Last time, we focused on the growth impact. This time, let’s talk about the current account.

In some ways, the effect is pretty obvious. Higher oil prices mean a higher oil import bill, which will mean a bigger current account deficit. How big? Well, a reasonable guess is that the deficit could double, rising from around 1 3/4 percent of GDP in the current fiscal year to somewhere between 3 and 4 percent of GDP in 2022-23, depending on how high oil prices go, for how long.

Let’s break this down a bit, using some round numbers. Next fiscal, GDP will be around $3 trillion in dollar terms. So, a current account deficit of 3 percent of GDP would be around $100 billion. Assume further that there will be enough private financing (through FDI inflows and external commercial borrowing, less FPI outflows) to cover about half of this amount. That would leave $50 billion to be financed. If the current account deficit turns out to be wider and private financing isn’t so forthcoming, the gap could even reach $100 billion.

Hmmm. That sounds like a lot of money. Where would the money come from to finance this balance of payments gap? Wouldn’t it be better to reduce the current account deficit?

Let’s examine each possibility. Start with the financing strategy. The RBI has some $630 billion in foreign exchange reserves. That means it could easily fund even a $100 billion gap in the balance of payments.

So, are we done? Nope. Here is where things really start to get interesting. Recall from the previous post that there is also an internal adjustment/financing dilemma. Say that the government also chooses the financing option: it keeps domestic fuel prices unchanged, cutting excise taxes and allowing the budget deficit to widen. In this case, we could say that India as a whole is choosing to finance the shock, rather than adjust to it.

How would the internal and external aspects of this strategy fit together? Rather neatly, in fact. The government would finance its larger deficit by issuing additional bonds, which would then be bought by the commercial banks. Meanwhile, the banks would finance the additional cost of imports by buying foreign exchange from the RBI, paying for these dollars using….the government bonds!

In the end, the government would be financing the increase in its deficit by selling additional bonds to the RBI. So, the RBI would wind up with more government bonds and fewer dollars, but with unchanged overall assets. Which in turn means that its liabilities — the money supply — remains unchanged. So, this process solves the external and budget dilemmas, without creating any inflationary pressure. Pretty cool, eh?

I know this sounds a bit like some complicated magic trick. It looks wonderful, but it’s so complex you are sure there must be some trick in there. So, let me go through the same process, but in a much simpler way. Essentially, what would happen under the financing option is that the government would run a larger deficit, which the RBI (which in the end is just a part of the wider public sector) would finance by running down its foreign assets. It’s just that simple.

But, um…yes, you are right to suspect a catch. There are at least three problems with a financing strategy.

First, relative prices in India would be distorted. And we know from past history what this means: India would end up wasting a precious resource, fuel, which would be bad for its competitiveness and bad for the environment.

Second, the government would end up further in debt. As a result, its interest obligations will increase, which will only intensify the budgetary squeeze, as these obligations already take up 43 percent of revenues, leaving very little room for productive expenditures.

Third, financing would impede external adjustment. Whenever India’s terms of trade deteriorates, the best response is to pay for the increased cost of imports by increasing exports. After all, India cannot respond by running down its foreign exchange assets forever. And there are major benefits to an export boom, most obviously in that it boosts growth. But the only way to generate this response is by making exporting more profitable, that is for the RBI to step back from foreign exchange sales and allow the exchange rate to depreciate.

So, now we can appreciate the dilemma. A financing response to the oil shock has advantages, but also some real disadvantages. It follows that the optimal strategy will involve a mix of both financing and adjustment. Some foreign exchange intervention, but some depreciation. Some fuel subsidies, but some passthrough.

Finding this delicate balance will be a major task for the government and RBI — probably their major task for the coming year.

A long, long time ago, in the 1980s, there was a British band called Depeche Mode. No one talks much about them nowadays, but at the time they were very successful. And one of their big hits was a song called “Get the Balance Right“. One of the verses went:

Don’t turn this way, don’t turn that way

Straight down the middle until next Thursday

First to the left, then back to the right

Twist and turn ’til you’ve got it right

Responding to a big shock is not easy. After the Global Financial Crisis in 2008, the government and RBI got the balance wrong. The result was a mini-crisis, with the government deficit soaring, inflation spiralling to double digits, and the currency plummetting. Of course, that was a different era. India is in a much better financial position now, with a very different government. Even so, getting the balance right won’t be easy.

Hang on to your hat.

Why Will High Oil Prices Curb Growth?

March 3, 2022

Why am I so worried that high international oil prices will derail India’s recovery? The nation wants to know!

Let’s start with a simple analogy. Say you are the owner of a kirana shop, taking in a tidy Rs 50,000 per month in profit. Now, imagine that suddenly your monthly profit falls to just Rs 25,000. What should you do about your spending? Should you just ignore this result, and carry on as before? Or should you tighten your belt?

The answer depends on the circumstances, doesn’t it? If you think that the monthly result is just a temporary aberration, you carry on. But if you discover that something fundamental has changed and that you are probably going to be earning Rs 25,000 from now on, then you really have no choice: you need to tighten your belt.

So it is with nations. The rise in international oil prices has increased India’s oil import bill by 1 1/2 percent of GDP. (See my previous post.) Think of this as as tax that foreigners have imposed on the country, effectively cutting the nation’s disposable income by the same amount.

Now, the nation needs to decide what to do. Following the logic of my example, one can conceive of two extreme cases.

One possibility would be to ignore the reduction in income and carry on spending as before. In that case, the gap between spending and income would need to be filled by borrowing. Someone would need to borrow an additional 1 1/2 percent of GDP.

How would this work? Most likely, like this: the government would keep domestic prices unchanged, reducing excise taxes to offset the rise in international prices. If the government decides not to take offsetting actions, the loss of revenue would increase the budget deficit, forcing it to borrow an additional 1 1/2 percent of GDP.

Is this a good idea? Well, it depends. The advantage of this strategy is that it protects the private sector. So, it is likely to carry on spending as before, allowing the economic recovery to proceed undisturbed.

The problem, of course, is that the government would go deeper into debt, which is… a problem when its debt ratio (centre and states combined) is already nearly 90 percent of GDP, just about the highest it has ever been in independent India. Clearly, then, this is not a strategy that the government will be willing to accept easily, particularly since this is not a temporary matter: oil prices are likely to remain high for some time.

So, recalling what our kirana shop owner would do in such circumstances, consider the alternative strategy of tightening one’s belt. How would this happen? Well, the government could respond to its loss of revenue by cutting its spending, so it can hit its budget deficit target and avoid going deeper into debt. Or it could pass on the price increase to the private sector, who likewise might decide to reduce their spending so they don’t go into debt.

The advantage of this strategy is that no one ends up in a debt problem. The disadvantage is that spending would be cut by 1 1/2 percentage of GDP, which will reduce growth.

Summarising and simplifying a bit, there are two extreme cases: zero impact on growth but a 1 1/2 percent of GDP increase in debt; or zero increase in debt and a 1 1/2 percentage point reduction in growth.

Of course, the reality is likely to be somewhere in between these polar cases. Most commentators expect, based on historical experience, that the growth impact will be toward the lower end of the range, perhaps even as little as 1/4 percentage point. But we should be wary of basing our predictions on historical experience.

The reason is that reactions depend on the overall macro context. For example, in the mid-2000s oil prices surged to nearly $150 per barrel but the private sector didn’t cut their spending plans at all, because they were convinced that India was going to be growing at 10 percent per year for the next decade. That meant that that they could easily ride through any dents in their incomes, since they would more than make up for these dents in subsequent years.

The situation now is very different. The private sector has just come through a very difficult patch, and remains anxious about the future, as the RBI’s consumer confidence survey reveals. Similarly, the government’s financial position is much worse than it was in the mid-2000s. So both the private sector and the government will react very cautiously to the decline in income.

To be clear: I am not saying at all that growth rate needs to be revised down by 1 1/2 percentage points. That is an extreme case, an exaggeration. But equally, the impact is not going to be zero, either. It is going to be significant. Very significant.

Consider yourself warned.

A Low Blow

March 2, 2022

When I was young, my parents used to tell me that you should never kick someone when they’re down. Actually, I’m quite sure they said I should never kick anyone, period. But they were especially emphatic that kicking someone when they were down was a low blow, indeed.

So, let me be clear: the rise in international oil prices is a very low blow. The economy is still struggling to recover from the pandemic (see the February 28th post below). And now the country will need to contend with a much higher oil bill. How much higher? I’ll get to that in a minute. But I need to make another point first.

Whether this is a serious issue depends on your view of how long oil prices will remain high. My view is that whatever the outcome of the Russian invasion of Ukraine, the sanctions on Russia will stay on for a long time. And though these sanctions do not actually forbid oil exports, they have made it so difficult for Russia to conduct trade that the international market will be short of oil for some time to come. In the past, other nations would have been able to compensate by increasing their own production. For example, the US itself was earlier able to step up its shale production whenever international prices rose. But there has been so little investment in the oil industry in the past few years that large production increases may now be impossible. As a result, oil prices are probably going to stay high for quite some time, possibly for several years.

Of course, that’s just a prediction. It may not come to pass. But let’s consider the implications if this scenario materialises. And let’s talk in really round numbers because, hey, we are speculating anyway. So, there’s not that much to gain by being precise.

Here goes. Last calendar year, oil prices averaged around $70 a barrel. Let’s say that this year they average around $100/barrel. In that case, the additional cost to India, rounding up a bit and also considering the impact of higher costs for fertilizer inputs, would be around 1 1/2 percent of GDP.

This is a huge number, so big that I should repeat it, in case it hasn’t sunk in: India could suffer an income loss of 1 1/2 percent of GDP.

What? You say, that doesn’t seem so big to you? Well, think of it in relation to some other numbers. Let’s say the budget deficit overruns the target by 1 1/2 percent of GDP. Or that growth falls by 1 1/2 percentage points. Oh. Now you see what I’m talking about.

The first question is: who will bear this income loss? Well, the government could force the private sector to bear the loss, by passing the increase in international prices onto domestic prices. But this would be very difficult to do. Already, incomes of ordinary people have taken a sizeable hit during the pandemic, even as many were saddled with extraordinary medical bills. So, it would be difficult to ask them to accept a further sacrifice in their standard of living.

But the alternative of asking the government to bear the cost would also be difficult. Consider that this fiscal year, in order to provide a modest 12 1/2 percent of GDP in goods and services to the country, the centre had to borrow 7 percent of GDP. Given this difficult fiscal position, how can the government afford to take on additional spending obligations? Especially when these obligations may not be temporary, but could last for several years.

Assume then that the government tries to muddle through, taking some of the income loss onto the budget but forcing the private sector to absorb much of the loss. That means that fuel prices will increase, spurring inflation. I’ve already pointed out that inflation is likely to remain dangerously close to the 6 percent upper limit of the RBI’s legally mandated inflation target. (See my post of February 12 below.) If fuel prices are increased, then the limit could be breached, in which case the RBI will be forced to raise interest rates.

Let’s sum up. Just a time when the economy is still trying to overcome the recession, a sharp rise in oil prices is hitting the economy from all directions:

- It will damage all the motors of growth, reducing household incomes and hence consumption; squeezing corporate profit margins and hence investment; and disrupting foreign economies and hence exports.

- It will also increase inflation, forcing the RBI to increase interest rates when it really would prefer to nurse the recovery.

- And it will put pressure on an already-weak fiscal position.

That’s quite a large kick to an economy that is already down. A low blow, indeed.

Where’s the Boom?

February 28, 2022

Well, that was a disappointment. GDP growth for December 2021 came in at 5.4 percent (year-on-year), somewhat less than what economists had been expecting and much less than the 7-9 percent that some people had been bandying about. Since over the course of 2020 the economy hadn’t grown at all, this means that over the past two years the economy has grown by just 5 percent. Very disappointing.

But we know this story. We know the economy was slowing down even before the pandemic hit. We know the lockdown hit the economy hard. And we know that ever since then the economy has been struggling to recover. What we don’t know is what the future holds.

Some people are very confident that a boom is on its way. Arvind Panagariya, the former vice-chairman of NITI Aayog, predicted just the other day that growth is sure to be 7-8 percent over the next decade, or even more if things go well.

Now, that sounds much better! So, what can we learn about the economy’s prospects from this GDP report? Let’s take a quick look at the numbers.

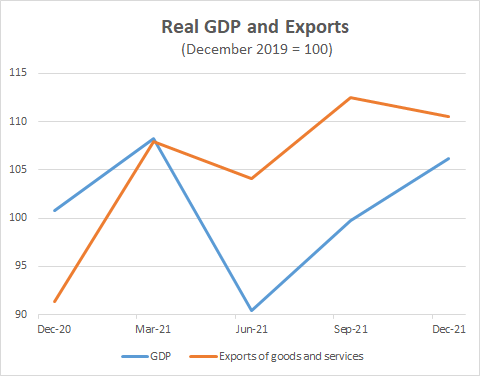

One of the key reasons why the economy has been able to grow over the past year is that exports have, ahem, boomed. Measured in the national income accounts way, that is calculated in real rupees and including both goods and services, exports have increased by a phenomenal 21 percent over the past year. Here is the chart. You can see how exports (in orange) have lifted the level of GDP.

But look again at the chart. On closer inspection, the GDP release sends a warning signal: in December, the level of exports actually declined. Of course, one shouldn’t get worked up just by one number. After all, exports do fluctuate from quarter to quarter, as the chart also shows. But we have some background information. We know that the global economy is slowing down: the IMF forecasts that world growth is likely to be 1.5 percentage points lower in 2022 than it was last year. And that forecast came out in January, before Russia’s invasion of Ukraine, which will only make matters worse. So, looking ahead, one of the key motors of India’s recovery could be sputtering to a halt.

In that case, we really need the other engine of sustainable growth, investment, to start revving up. What have we learned about investment from the GDP release? Nothing good, I’m afraid. Here’s the chart.

You can see the problem. There are just no signs that investment is taking off. In fact, gross fixed capital formation (what ordinary people mean by investment, that is excluding stock building and accumulation of gold holdings) actually fell during the third quarter.

So: one engine is sputtering and the other hasn’t even begun to turn. Hang on. It’s going to be a bumpy flight.

RBI’s Inflation Forecast, Again

February 24, 2022

The other day, Deputy Governor Patra made some interesting remarks at the Asia Economic Dialogue. He explained that the RBI is confident that inflation is headed toward 4 percent because supply constraints are easing. He noted that “the New York Fed’s global supply chain pressures index is peaking and is set to moderate from hereon.”

This comment is interesting, for three reasons.

First, Patra focused on supply, rather than demand. Most commentators have done the opposite, arguing that the problem is low demand. They cite the exceptionally low capacity utilization rate of 68 percent (in the third quarter of 2021-22) as evidence that there is plenty of unused supply.

But there are huge holes in the conventional argument. Just because factories are not working to full capacity doesn’t prove that demand is the constraint. In fact, there is at least one major industry where we know this isn’t the case: automobile manufacturing, where firms are unable to produce because they cannot get needed inputs from abroad, notably computer chips. Similarly, production by other firms was hit hard in the third quarter because they weren’t able to secure the coal supplies they needed.

Perhaps most important, if the problem is weak demand, then why didn’t inflation collapse during the pandemic? Let’s bring back the chart I first showed a few days ago. As you can see, core inflation actually increased after the lockdowns, suggesting — yes — that there must have been a problem with supply.

If inflation has been caused by supply constraints, what are the implications for monetary policy? Patra’s second point is that monetary policy can’t fix supply chain problems. So, the RBI shouldn’t worry about inflation; it should focus instead on stimulating growth.

But surely this gets things the wrong way around. If supply is constrained, then monetary stimulus can’t do anything to increase output; it can only generate inflation by propelling demand above the level of available supply. In other words, high inflation suggests that policy needs to be tightened so that aggregate demand is brought down to the level of available supply.

There is, of course, an important exception to this rule. And that brings us to our third point. Patra argued that in this particular case monetary policy doesn’t need to do anything because the supply constraints are temporary; they are going to be easing in coming months. So, inflation will fall naturally, even without any monetary policy tightening.

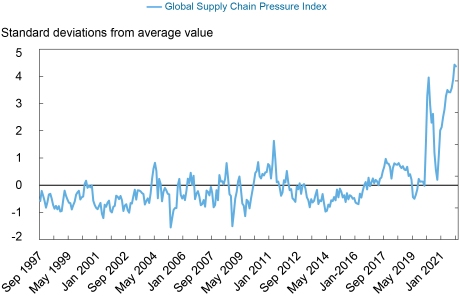

He bases this claim on the Fed’s measure of supply chain problems. So let’s take a look at the Fed’s index.

You can see a few points clearly. The current level is exceptionally high, meaning that the supply constraints are still very severe. And there’s no sign that the index is turning down. To the contrary, there are reasons to think that the supply problems are actually going to get worse: the Russia-Ukraine conflict, for one. Recall that these two countries are major exporters of raw materials, not just of energy, but of key products needed for, say… computer chips. For example, some 90 percent of the world supply of neon, used as laser gas for chip lithography, comes from Russia and Ukraine.

So, again, how can we be so confident that inflation is headed to 4 percent?

The Return of Fiscal Dominance

February 22, 2022

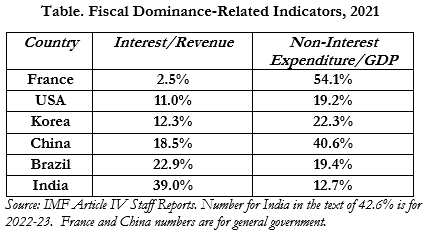

Just think about this for a minute. The centre devotes more than 40 percent of its revenues to meeting the interest payments on its debt, an extraordinarily high level compared to other major countries, advanced or emerging.

As a result, in order to spend a mere 12½ percent of GDP in the 2021-22 budget on investment, social sectors and defence, the central government had to run a deficit of 7 percent of GDP.

These two sentences tell you all you need to know about the state of the public finances. It is worrisome, very worrisome indeed.

Somehow, the government will find a way to muddle through. But the difficult fiscal situation will impose a heavy constraint on monetary policy in the coming years, since the government cannot really afford to allow the RBI to increase interest rates. So how will the RBI be able to fulfill its mandate of maintaining price stability?

Arvind Subramanian and I explore the fiscal/monetary dilemma in a column in today’s Business Standard.

Does Reducing Imports Increase GDP?

Perhaps you saw the recent SBI report, which claimed that reducing imports from China would increase GDP. I didn’t; I only saw the summary in the newspapers. But if the PTI summary is accurate, the authors have made a mistake.

It’s a common mistake, because the math seems so compelling. Imports from China are in areas covered by the PLI initiative are around $40 billion. Hence, the report (and headline) claims that “India can add $20 billion to GDP if dependence on China is halved”.

The logic seems straightforward. When the various elements of the national income accounts are added up, imports are subtracted. So if consumption, investment, and exports equals 100 and imports are 20, then GDP is 80. It seems to follow that if the 20 could be eliminated, then GDP could be increased to 100.

But there is a big problem with this logic. In fact, two problems. First, if imports change in the national income accounts, something else will change. After all, the imports are used for something: they are consumed, or used for making exports, or used for investment projects. Let’s say they are consumed. In that case, if imports go down by 20, then consumption goes down by 20. GDP is still 80. This is just the way the accounting works.

Ah, but I here you say, “This is not what I have in mind at all. My idea is that India replaces the imports with 20 in domestic production. Then GDP will indeed go up by 20.” Well, not necessarily.

So, consider the second way in which the claim is wrong: it fails to consider how economies actually work. Consider a simple example, using a single firm to represent the entire economy. Let’s say that this firm imports cloth for 20 and transforms it into a shirt, which it exports for 100. So value added (that is, GDP) is 80. Let’s assume 70 of this value added goes to meet labour and other expenses, and 10 is left as profit.

Now, assume the government imposes a large tariff on cloth imports, so that the firm needs to buy domestically at a price of 35. This is a problem, as the increase in costs of 15 has just wiped out the firm’s profit of 10. So, the firm may need to close.

But wait! Assume the government then comes in with a subsidy of 20, to compensate the firm. So, everything is fine, right? In fact, the firm is better off than before. Its profit is now 15, so it will want to expand!

The problem is that the government can’t create the 20. It needs to get it from somewhere, say by taking 20 as tax from the firm. So, now the firm is in the same situation as before. Its net costs have increased by 15 and it has to close.

One could come up with more complex examples. For example, if you assume there are two firms, then it is possible that the shirt exporter will not be taxed, so it will be a net beneficiary of the scheme. But then some other firm is bearing the tax burden, and its production will contract, most likely by more than the first firm is expanding. So, on balance, GDP will fall.

There is one case where this strategy might just work. Let’s say that the increase in costs from shifting to domestic cloth production is small; and that over time, as domestic production of cloth expands, the production cost is lowered to world levels. In that case, everything will work out.

But what are the chances of that? India has seen many cases of firms that grew up on the basis of tariffs and subsidies. Many, many of them were completely unable to become internationally competitive. One just has to think of the car industry, pre-liberalisation. Or the efforts to promote domestic production of computers in the 1980s, which set back India’s efforts to join the computer age for a decade.

But let’s return to the claim of the SBI report. The point is simple. No, reducing imports does not automatically increase GDP. In fact, it is much more likely to reduce it.

Thinking the Unthinkable

February 14, 2021

Remember the good old days? The days when India was the fastest-growing economy in the world, the envy of all the other countries. How wonderful it was to be alive!

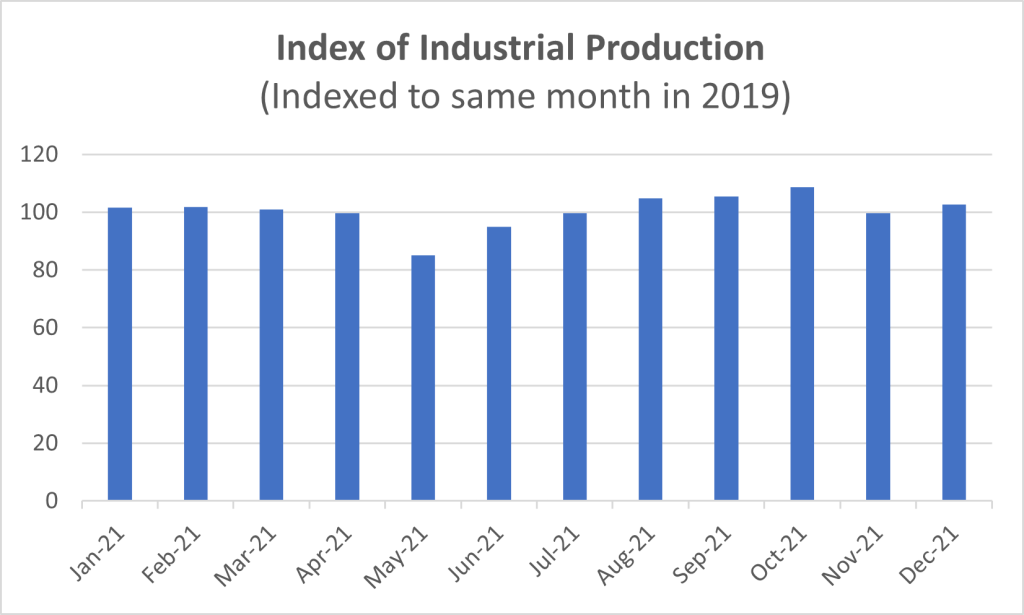

But that was… two weeks ago. Then came last week’s IIP numbers, slapping us with the force of a monsoon in the Western Ghats. IIP increased by only 0.4 percent, while capital goods production was even more disturbing, falling by 4.6 percent.

Of course these are year-on-year numbers, and we know that strange things were happening in 2020. So perhaps these are all just base effects?

Unfortunately, no. The chart above compares industrial production to its level in the corresponding month of 2019, the year before the pandemic arrived. You can see that production fell sharply when the delta variant hit, then started to recover. But then it slipped back in November, even before the omicron wave hit in December. So, no, there’s still no sign that a strong recovery is underway.

Perhaps we just need to be patient. Perhaps the boom is just taking a bit longer to materialize. But while we wait it is worth thinking about a “Scenario B”. What happens if the recovery is is deferred for a long time, or arrives soon but proves much weaker than we hope?

There’s no way I can examine all the implications in one blogpost. But let’s start by discussing one small aspect: the implications for social spending in the 2022-23 budget. Many commentators have noted that the NREGA allocation was reduced by Rs 25,000 crore compared to the revised estimate for 2021-22. Less attention, however, has been paid to an even larger spending cut, the (approximately) Rs 80,000 crore reduction in food subsidies. This reduction is premised on the assumption that the program of providing an additional 5 kg of rice or wheat at no cost to 80 crore people will be discontinued at the end of this fiscal year.

There’s no doubt that the government really wants to do this. But will they really be able to do so?

To understand the government’s quandary, we first need to recall why this program was instituted in the first place. It ‘s there not because the government likes to give away free food. They don’t. Rather, the program is meant to address a serious social problem. When the pandemic came to India, an estimated 32 million workers left the cities and went back to their villages, to work on family farms. This additional labour has helped increase agricultural production, but only a bit, since there was already excess labour in the countryside.

As a result, the rural areas had essentially the same amount of food but many more mouths to feed. This created a problem, a big one. The government was forced to step in and provide additional rations, to ensure that everyone had enough to eat.

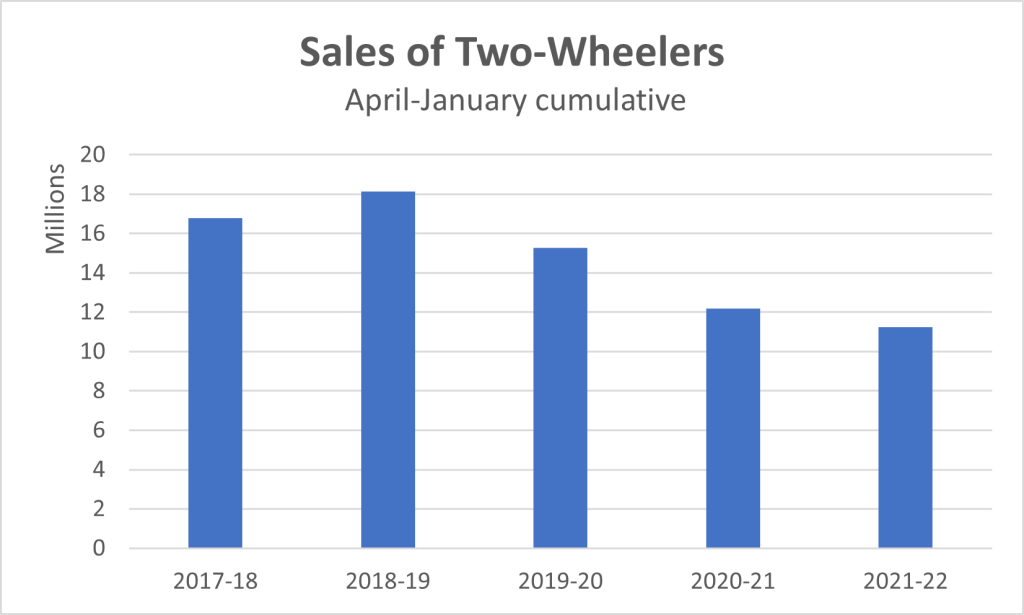

Even then, farm incomes had to be stretched to cover many more people. And just at the same time, the rising cost of inputs (see the February 10th blogpost) was forcing consumer goods firms to increase their prices. So, families were forced to cut back on their purchases. In the third quarter, major consumer firms like Hindustan Unilever and Darbur reported that sales volumes grew by only 2 percent off a depressed year-ago base, while sales at Bajaj Consumer Care fell by 6 percent. Only Britannia reported a reasonable growth, of 5 percent year-on-year, as people replaced more expensive food with biscuits.

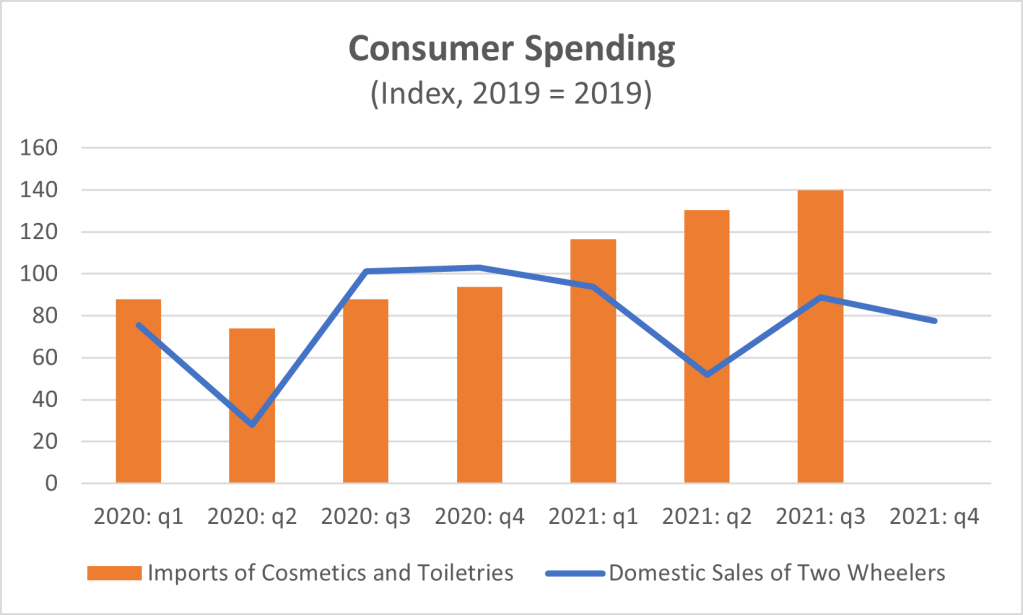

With some consumers finding it difficult to purchase soap and shampoo, major purchases are simply out of the question for many rural families. Consequently, sales of two-wheelers have collapsed. The chart below shows sales volumes so far in the fiscal year, compared to the same period in previous fiscals. You can see that the stress actually started in 2019-20, when the economy really slowed down. And every year since then it has only become worse. Sales are now at a 10-year low.

This brings us back to the outlook. When the government started its free food program, it assumed that the urban-to-rural migrants would go back to their old jobs when the economy rebounded. But so far there’s little sign of this happening. There’s no mass movement back to the cities. Nor are people able to get jobs in the countryside. So, what will the government do if the recovery continues to be delayed? Recall that the free food programme is meant to expire next month.

If that prospect isn’t worrisome enough, consider what might happen if the recovery materialises but proves very weak. There’s a risk, after all, that the pandemic will leave lasting scars. Put another way, perhaps the reason why the ‘reverse migrants’ haven’t returned to their jobs is that their jobs no longer exist. Many of these people worked for informal firms which have now closed forever, victims of the triple shock of demonetisation, GST, and the pandemic lockdowns. In other cases, they worked for firms which have survived, but which only managed to do so by downsizing, cutting their payrolls sharply.

All this means there’s a risk that people might need to stay back in the rural areas, depending on free food and NREGA, for quite some time. In that case, government spending could be much higher than budgeted, perhaps Rs 1 lakh crore higher, if both food subsidies and NREGA need to be restored to their 2021-22 levels.