We’ve all been there. We’re relaxing at home, just having a quiet night, when suddenly we hear a loud thump. So we turn to the person next to us and ask, “What’s that sound?” We try to sound confident-but-inquisitive, but the question doesn’t come out that way. Our voice is a bit shaky, revealing that actually we’re rattled. Very rattled. And it really doesn’t help when the other person says, in an equally shaky voice, “Um…I…I don’t know.”

That’s exactly where we are with the US economy. Until the other day, the economy seemed to be humming along. The service sector was reviving as Covid was ebbing, businesses were hiring workers as fast as they could find them, and — wonder of wonders — many people were actually going back to office! With all these good things happening, what could possibly go wrong?

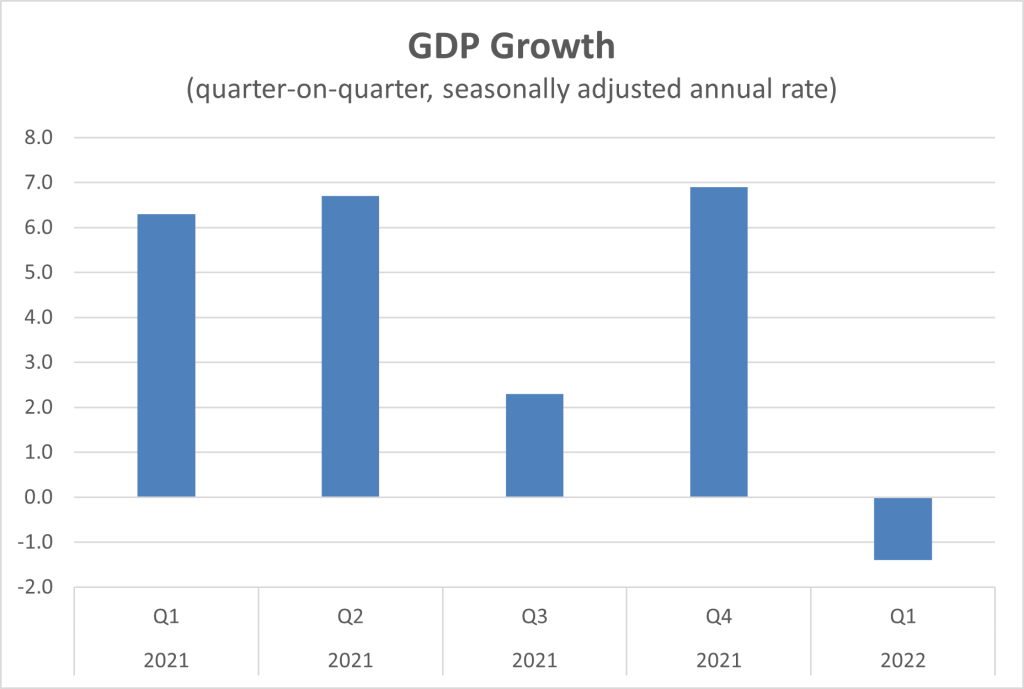

Evidently, something. Because last week the US government delivered the news that the economy actually contracted in the first quarter of this year. By 1.4 percent. This was a surprise, even to the people who spend their entire lives tracking the economy. Just a few days before, forecasters had predicted, shall we say, a more positive result. So, the news was the equivalent of a sudden thud in the middle of a calm night.

Should we be afraid? Absolutely, positively not, said the government, insisting that the contraction was merely the result of “technical factors”. Hmmm. Perhaps we better take a look at those technical factors. According to the New York Times, the main culprit was the ballooning trade deficit which “took more than three percentage points away from G.D.P. growth”.

Oh. That doesn’t sound like a technical factor. That sounds like a problem, and a big one. Why did the New York Times (and many other publications; I’m just using them as an example) say that the trade deficit took away all of America’s growth — and then some?

To answer this question, we need to understand the framework they are using. In economics, students are taught the following equation:

GDP = Consumption + Investment + Government spending + (Exports – Imports)

This is actually an accounting identity, saying that production must respond to the four sources of demand: from consumers, firms, government, and foreigners. You know, supply must equal demand.

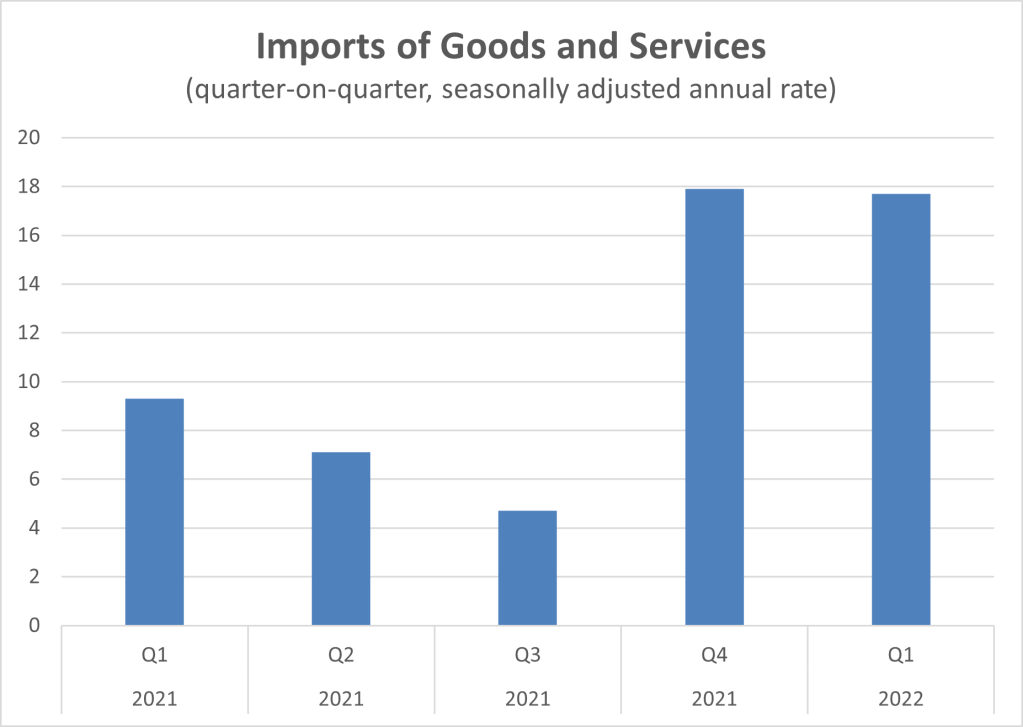

From this equation, one can easily see that if net exports (exports minus imports) go down — and nothing else changes — GDP will go down. And what happened in the first quarter? Yup. There was a very large increase in imports, on a swollen base, since imports had already increased substantially in the previous quarter. That’s why the NYT blames the trade deficit for the fall in GDP.

But is this interpretation correct? Look again at the equation. There are actually two possible cases. Imports could be substitutes for domestic domestic production. In that case, if imports go up, domestic production (GDP) will go down.

But that’s not true if imports are complements, that is vital components of domestic production. To take a current example, think about semi-conductors, which are almost entirely produced abroad and are currently in very short supply. If foreign firms ramp up their production capacity and the US is able to import more semiconductors, this will allow the US to ramp up its production of all sorts of products, ranging from cars to garage doors. In this case, an increase in imports will increase — not reduce — GDP.

How do we show this second case, in terms of the equation? Consider the following rearrangement of terms:

Consumption + Investment + Government Spending + Exports = GDP + Imports

This version just puts imports on “the other side”. But see the subtle shift implied by the rearrangement of terms? There’s no longer any implication that imports reduce GDP. Instead, we merely consider the level of demand (on the left hand side), and the two ways that this demand can be met: through domestic production (GDP) or imports.

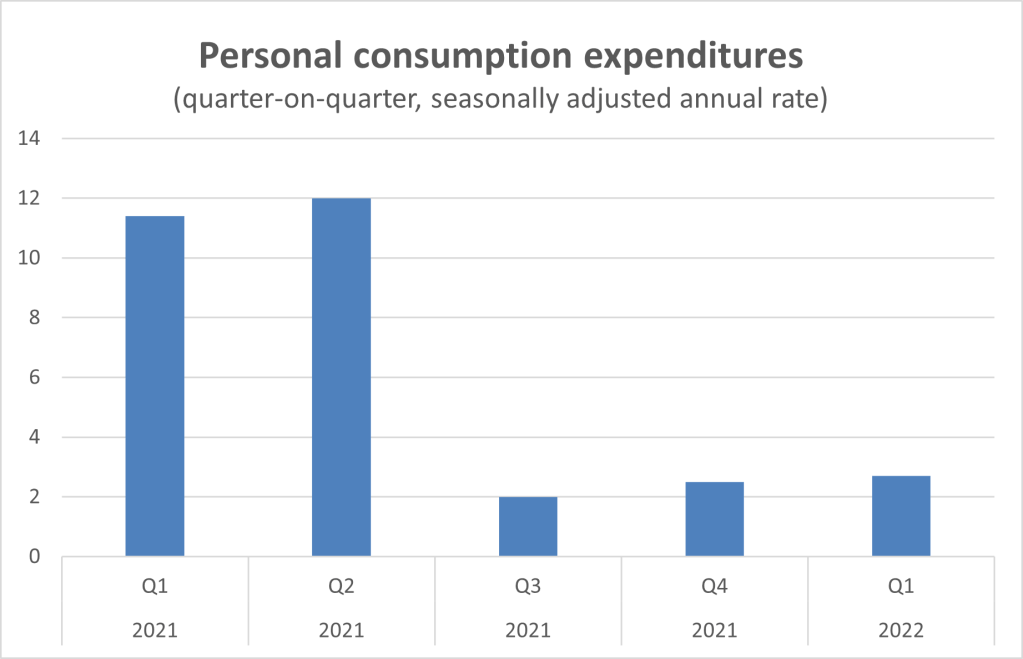

Armed with this framework, let’s try to answer the implicit questions. First, how is demand doing? Let’s look at consumption, which accounts for about two-thirds of aggregate demand. As the chart shows, consumption is far from weak; after the economy normalized (from the Covid lockdowns) in the third quarter of 2021, it has actually been accelerating.

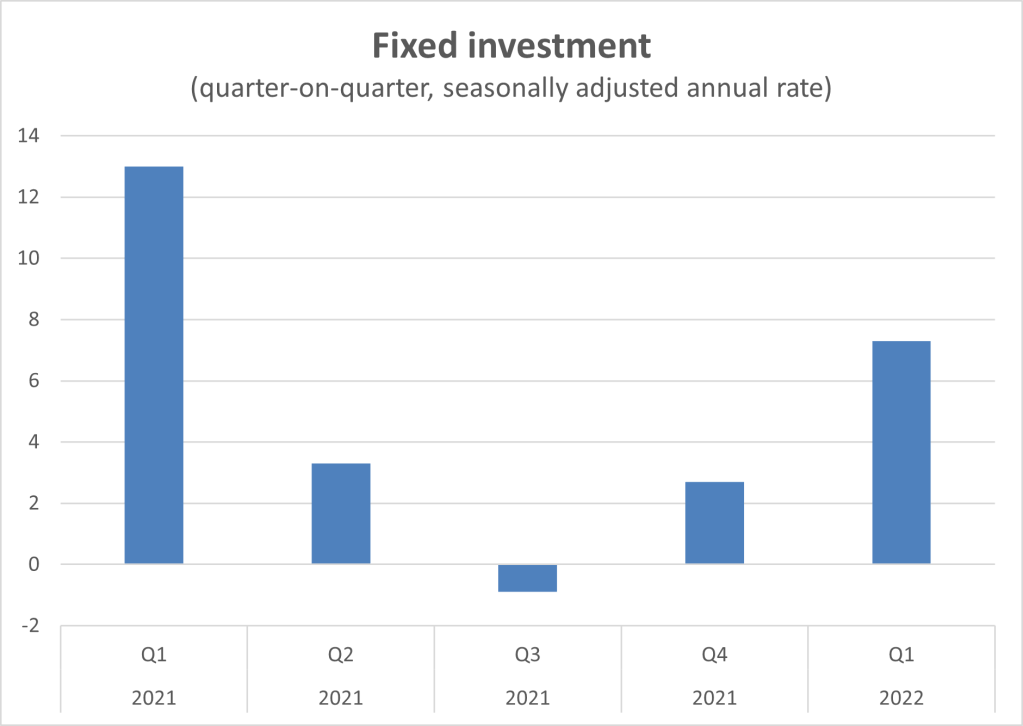

What about business investment? Same. It is also gaining strength.

There are some other things going on. For example, the government is winding back its pandemic-related spending. But you get the picture. Private sector demand is not weak at all; it is actually quite healthy.

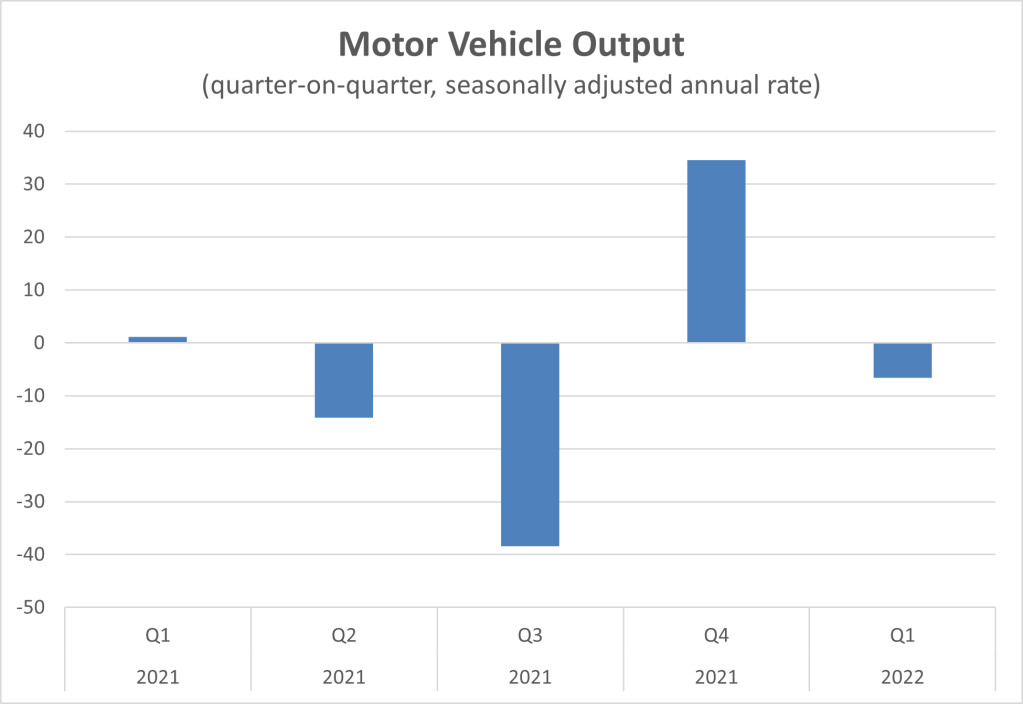

So, why then, did this demand not translate into more production? The reasons are still not clear. But part of the problem relates to the “supply chain crisis”. That is, businesses still cannot get the parts or even the workers that they need to expand production. You can see this problem clearly in the automobile industry, where production has been sputtering, despite strong demand for cars;

Here’s the thing. If production is supply constrained, then the increase in imports is a good thing. It means relief is on the way, in the form of greater supplies of needed inputs. This increase in supplies should allow production to rise in subsequent quarters, especially for manufacturing and construction.

In this case, there’s no need to worry about that thud. But of course we don’t know this for sure. After all, loud thuds are sometimes signs of further, truly worrisome thuds to come. So, we need to be alert.

In the 1960s, Buffalo Springfield warned us:

“There’s something happening here

But what it is ain’t exactly clear…

I think it’s time we stop

Children, what’s that sound?

Everybody look, what’s going down?”

Perhaps we need to stop and listen again now.