Have you ever taken a train that’s heading in the wrong direction? If you have, you know what unfolds. First comes the confusion, the strange feeling that something is wrong, even if you can’t quite put a finger on it. Then comes the gradual realization that uh-oh, you’ve made a dreadful mistake. You’ve wound up in the wrong place, your schedule is now all messed up, and it’s not clear how you are ever going to get back on track.

Something like this might be about to happen to most Americans. For more than three decades, Americans have put their faith in the Federal Reserve to keep the economy on the path of low inflation. And that faith has proved completely warranted. An entire generation of Americans hasn’t had to bother about inflation. No consumer rushes to the stores to spend their paycheck before prices go up. No business scales back its investments because costs are too difficult to predict.

Sure, people used to do these things in the US…way back in the 1970s and 1980s. And sure, they still do them in places like Zimbabwe. But they do not do such things in 21st Century America. Certainly not.

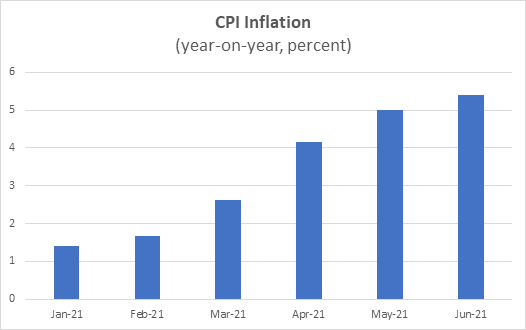

But this year strange things have started to happen. Every month, inflation has crept a little bit higher. It started the year at a modest 1 percent. But then it passed 2 percent, 3 percent, 4 percent, and even 5 percent, reaching 5.4 percent in June.

This progression has started to unnerve some people. So, their eyes have turned to the Fed, to see what it is going to do to stop inflation in its tracks.

And how has the Fed responded? By doing precisely…nothing. It has maintained its short-term policy rate at essentially 0 percent, while continuing to push long-term rates down by purchasing $120 billion in bonds every month. And it has made clear that it is not planning to change course any time soon. Fed Vice Chairman Richard Clarida said just last Wednesday that the central bank could announce its intention to begin raising rates… in 2023.

What on earth is going on? Why isn’t the Fed reacting? Have Americans made a massive mistake, thinking that they were on the low-inflation train, whereas they are really headed on a nonstop flight to Zimbabwe?

Until recently, there was a pretty good answer to this question. And like all good answers, it was simple and clear. The answer was: no. An emphatic no. The Fed wasn’t responding to this year’s inflation figures because… there didn’t seem any need to respond to them.

You see, the inflation figures have been highly misleading. Sure, prices were increasing sharply, but to a large extent they were just normalizing after a bizarre 2020, when Covid arrived and prices collapsed. Think of apartments in New York City, where landlords in 2020 were so desperate that ordinary people – imagine, ordinary people! — could suddenly afford to rent beautiful two-bedroom apartments in the best neighborhoods. We all knew this situation was too good to last, and indeed it was. As New York has come back to normal, so have apartment rents. And airline fares. And many other prices.

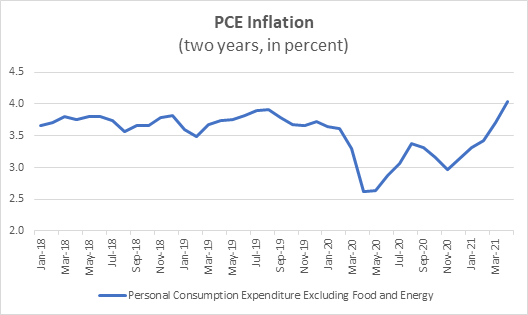

Take a look at this chart, which puts some numbers on the phenomenon. It shows inflation, not in the usual year-on-year way but rather over the span of two years, so the figure for February 2021 (for example) shows the price increase since February 2019. Also, instead of using the CPI, the chart uses the Fed’s preferred index, which measures prices for personal consumption expenditure, excluding the volatile categories of food and energy.

This chart does not show any surge in inflation. Rather, what is striking is the fall in inflation during 2020. This year, inflation (measured in this manner) has merely returned to a normal 4 percent, that is 2 percentage points per year.

So, nothing to worry about? Umm…not so fast. I deliberately ended the chart in April 2021. Since then, the picture has changed, pretty radically in fact. So let’s add the last two months and zoom in on just the current year. When we do this, the picture looks amazingly like the first graph. Over the last two months inflation is definitely higher than normal, and the trend doesn’t look good.

So, why hasn’t the Fed responded now? The answer is that they don’t buy any straight-line extrapolations that have the US ending up like Zimbabwe. They are convinced the trend won’t last, that supply disruptions will naturally fade away as the economy continues to open up and people go back to work.

But will they? This is certainly possible scenario. But it is not the only one, or even necessarily the most likely one. As I mentioned in my previous blogpost, the economy has been opening up for the past few months, but supply disruptions are not easing. They are in fact getting worse. Much worse.

So it’s worrisome that the Fed is not “taking out any insurance”, by tightening its stance just in case the inflation pressures prove more prolonged that they currently expect.

Actually, when I said earlier that the Fed has done nothing, I wasn’t completely correct. In fact, the Fed has changed its stance: it has loosened the stance of monetary policy.

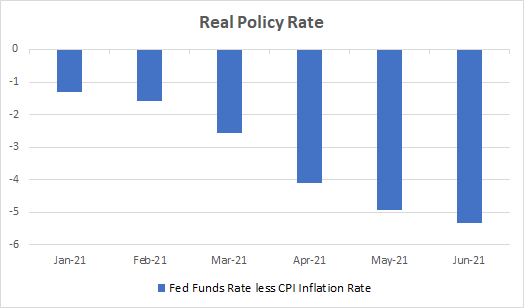

You see, one can’t measure the stance of monetary policy by looking at nominal interest rates. One needs to consider the inflation rate. After all, a nominal interest rate of 10 percent is pretty high if inflation is 2 percent, but extremely low if inflation is 20 percent. If we consequently look at policy rates in real terms, this is what we see:

The chart exaggerates the problem, because it compares a forward-looking interest rate with a backward-looking inflation rate. And the whole issue is whether the current inflation will continue. But ignore these technicalities, as they are the kind that only an economist can love. The broad point remains: the Fed has responded to rising inflation by reducing its real policy interest rate, driving it further and further into negative territory.

At this point, the Fed is essentially offering you free money. That is, you can borrow money at very low rates, buy some goods, hold them, wait till prices go up, then sell them and make a handsome return, more or less risk-free. Is it any wonder, then, that the stock market and housing prices are soaring? That people are even speculating with used cars?

But I digress. The point I want to make is that, by reducing real rates, the Fed has been injecting even more stimulus into the economy. This is of course on top of the massive fiscal stimulus already being provided (and planned) by the Federal government. Taken together, these stimuli will increase demand mightily at a time when the economy is plagued by supply problems.

Put starkly, the Fed – for the first time in a generation – is placing a major gamble on the future of the economy. If its scenario is correct, the stimulus will pay off handsomely. The economy will take off, the supply problems will disappear, and inflation will fade away. But if their call is wrong, the stimulus will create a major, protracted inflation problem.

So are we headed to Zimbabwe? No, I still don’t think so. But we could be headed back to the 1970s. And that would be bad enough.