Everybody likes a good summer mystery. Especially the really mysterious ones, where you can’t even figure out what on earth is going on. You know, like when a troublesome creature from the past suddenly turns up again, rattling people who wonder why he’s come back, how long he plans to stay, and how much trouble he is going to cause in the meantime.

So consider the real-life case of the returning inflation. For more than two decades, inflation had vanished from the US economic scene. But suddenly this summer it has returned. And everyone wants to know why.

Fortunately, someone claims to have cracked the case: the vaunted Inspector Fed. And he has good news to tell us. He is convinced there’s nothing to worry about, because inflation will be gone soon. Real soon. Without Inspector Fed even lifting a finger.

That’s great news – if the Fed is correct. But is it? Let’s look closely at the case.

Why is the Fed so convinced that inflation is transitory? Essentially, because it believes the current economic situation is transitory. The Fed argues that the economy was disrupted by the lockdowns of 2020, and as the country opens up again everything will return to normal. Including inflation.

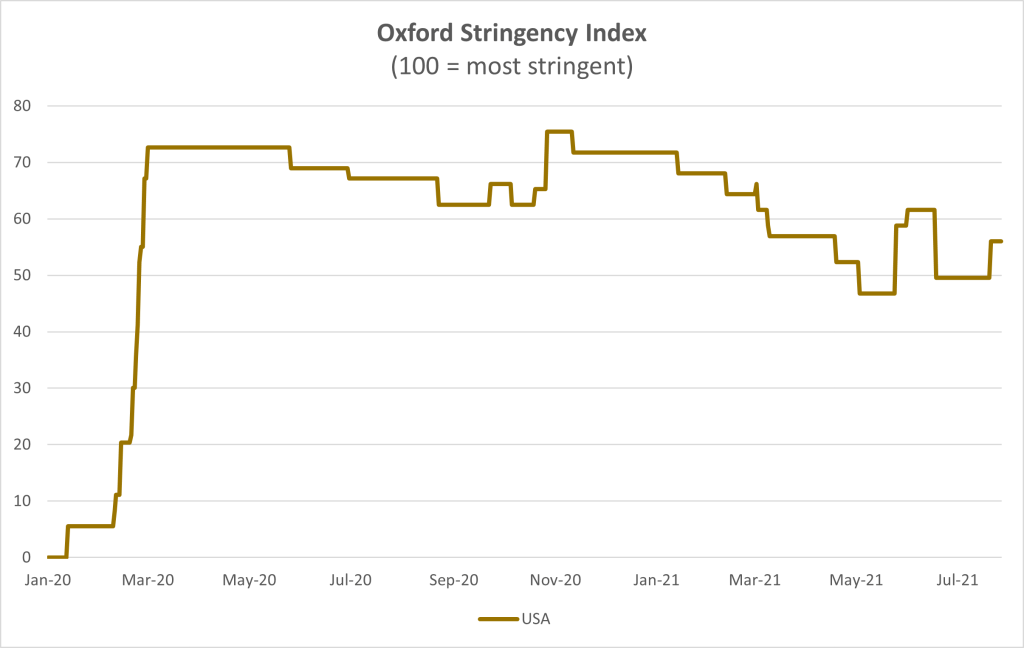

For evidence of this, take a look at the following graph. It shows the Oxford Stringency Index, a measure of the intensity of restrictions that were put in place after the pandemic hit the US in early 2020. You can see clearly that the restrictions were ramped up quickly but have only been eased slowly. We still have a long way to go before things return to normal. So, yes, we are still in a transitional period.

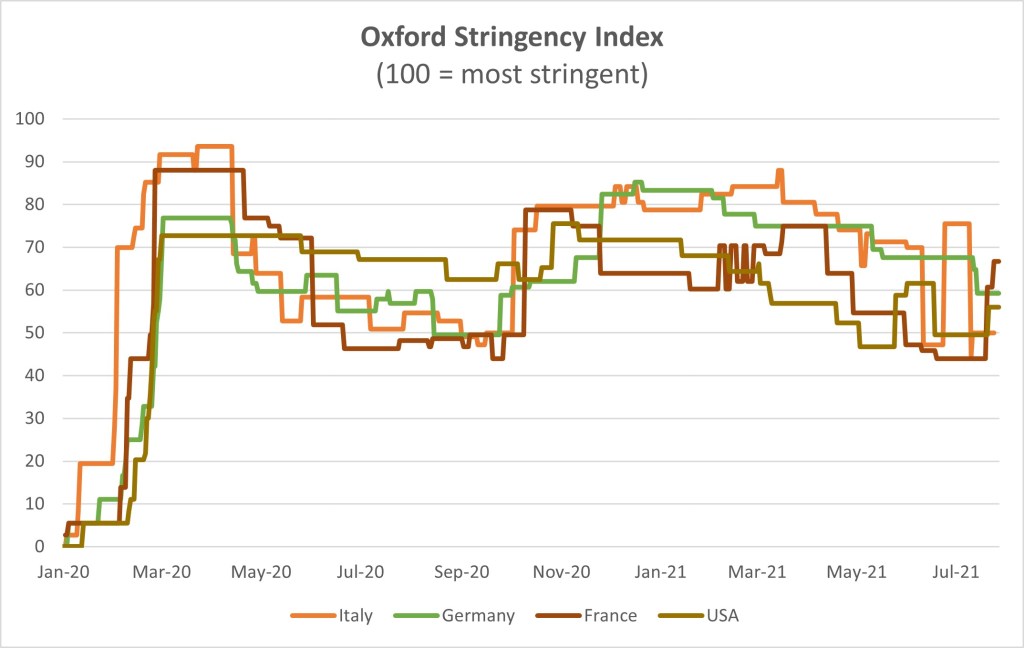

But here’s the thing. The U.S. wasn’t the only country to impose restrictions. Pretty much every country in the West imposed restrictions, too. You can see the story in the following graph. But don’t look too closely. You’ll really hurt your eyes trying to follow the path of each line.

And that is precisely the point. By and large, all the major Western countries imposed similar restrictions at the same time, then followed similar paths toward a cautious re-opening. Actually, if you want to be pedantic, Europe has even been a bit more restrictive than the US. But let’s not get pedantic. Ok, if you insist, because you are a truly nerdy type and won’t read further before finding out how this stuff is measured, take a look here.

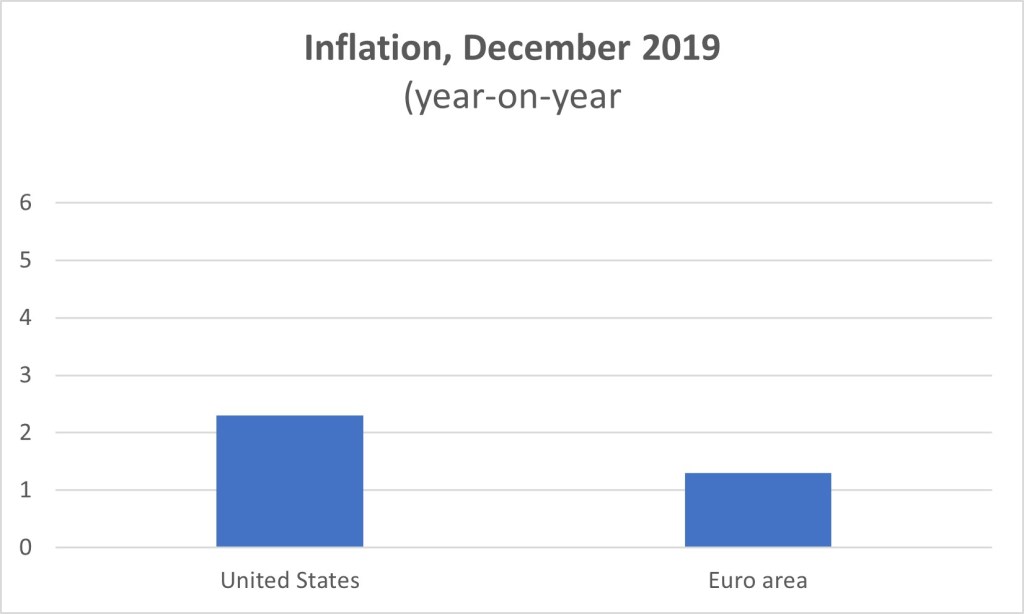

Now for the second point. Before the pandemic started, the US and the Euro area had similarly low inflation.

Let’s sum up the case so far. We have two data points:

• The US and the euro area started at more or less the same level of inflation.

• They took more or less the same Covid measures.

So let’s employ some Sherlock Holmes-type deductive reasoning.

• If the extra inflation has been generated by the Covid measures, as the Fed claims, then the inflation rates in the US and the euro area should still be about the same.

But they are not. They are not even close. The US inflation rate is more than double that in the euro area.

How can we explain this difference? Hmm. This is a difficult one. It could be that the US economy is more fragile than Europe, and more easily disrupted by lockdown measures. But does that seem plausible? Ummm. No, I didn’t think so, either.

So let’s consult our economics textbook to see if it might be able to help us. Oh, yes, there it is. Right there in the beginning of the book, in the chapter on inflation. It says that inflation is affected by the stance of macroeconomic policies. In particular, if stimulative monetary and fiscal policies lead to too much spending at a time when supply is constrained, say because the economy is coming out of a lockdown, then there will be excess demand and prices will rise.

Ok, then. That could give us some clues. If the macro policy stance in the US is more stimulative than that in Europe, this might be able to explain the difference in inflation.

Start with monetary policy. Is there a difference between the stance of the Fed and the European Central Bank? Well, no, not really. They are both pretty lax.

What about fiscal policy? Ah, now there’s a difference. A large one. The US fiscal deficit is projected by the IMF to soar to around 15 percent of GDP this year, more than double the level projected for the euro area.

Uh-oh. As Sherlock Holmes once said, “The game is afoot.”

Has the Fed possibly missed a clue, hiding in plain sight? And if the fiscal deficit is likely to persist, what are the chances that inflation will be transitory?

Asking for a friend.