March 22, 2023

Many years ago, there was a baseball player named Yogi Berra. Ok, Yogi wasn’t actually his first name: his real name was Lawrence. But everyone called him Yogi, because when he was a teenager someone decided he looked like a yogi. And the name stuck.

Yogi played for the New York Yankees in their glory days of the 1940s, 1950s, and early 1960s, when they were the best team in the most popular sport in America. He wasn’t actually the best player on the team, but he was one of the most popular, so much so that Hanna-Barbera named a cartoon character after him.

Here he is: Yogi Bear. Kids loved him.

But for all Yogi’s qualities, he didn’t get much respect from adults. They found him inarticulate and prone to stating the obvious in the most redundant of ways. Many of these malapropisms were simply invented by others and attributed to Yogi. At the time, this seemed unfair, leading Yogi to complain, “I really didn’t say everything I said.”

But decades later, Yogi got his revenge. Long after most players from the 1940s were forgotten, he received a Presidential Medal of Freedom from Barack Obama, because his sayings had become part of American culture.

Which brings me to the events of the past two weeks. Everyone who has been watching the dramatic developments in the banking sector has been having a Yogi Berra moment. It really does feel, as he once said, like it’s deja vu, all over again.

Specifically, it feels like 2008, all over again. And that’s not just because the first major bank collapse, Bear Stearns, happened 15 years ago last week. It’s because of a whole series of unfortunate events.

You know what I mean. First, there was an unexpected failure of a medium-sized bank that many people previously hadn’t even heard of. That led to a government bail out, followed by a strident insistence, from the President on down, that we should just move along, nothing to see here, since this was a special case and the other banks were perfectly sound. These statements were followed, of course, by further failures and bailouts.

As I said, a whole series of unfortunate events.

So, is this 2008 all over again? Is the entire banking system about to melt down, taking the overall economy with it? Answering this question is not easy. As Yogi reportedly once said, “It is difficult to make predictions, especially about the future.” Still, we need to try. So, let’s give it a go,

The first point to make is that, no, this is not the same as 2008. In fact, if we compare the two situations, we can see some major differences.

Let’s start with the good news. Back in 2008, the banks got into trouble by giving money to people to buy houses that they couldn’t actually afford. When it turned out — surprise! — that these people couldn’t actually repay the loans, pretty much every bank got into trouble.

This time is different, in two fundamental ways. First, the ultimate source of the banking stress is different. Since the 2008 crisis, banks have been much more careful about incurring credit risk (i.e., lending to people who can’t repay). So, when the pandemic hit and the government started depositing “stimulus checks” in households’ bank accounts, banks ploughed the money instead into government bonds, which were free of credit risk, because the government won’t default.

In doing so, however, banks incurred interest rate risk, because when interest rates go up, bond prices go down. At the time, banks didn’t worry too much about this risk, because there didn’t seem much prospect of the Fed raising interest rates aggressively. After all, inflation had been dead for 40 years.

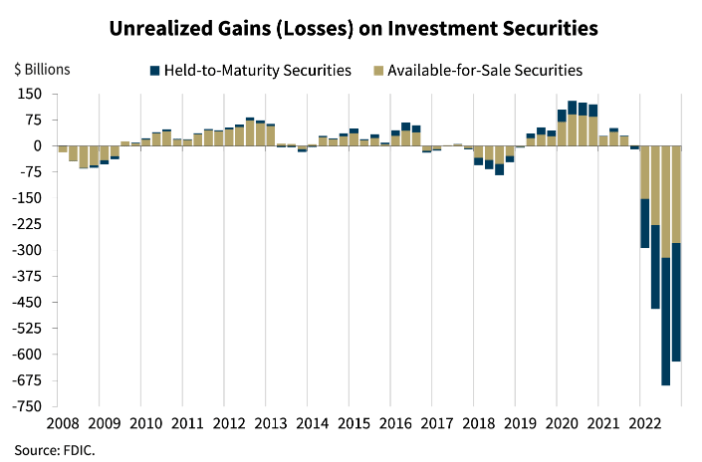

During the pandemic, however, inflation came back from the dead, forcing the Fed to raise interest rates, which meant that banks have suffered huge “mark to market” losses on their bonds. The FDIC (which insures bank deposits) has calculated that banks were sitting on more than $600 billion of bond losses in December 2022. That means that banks have effectively lost about 30 percent of their $2 trillion in capital. Not good.

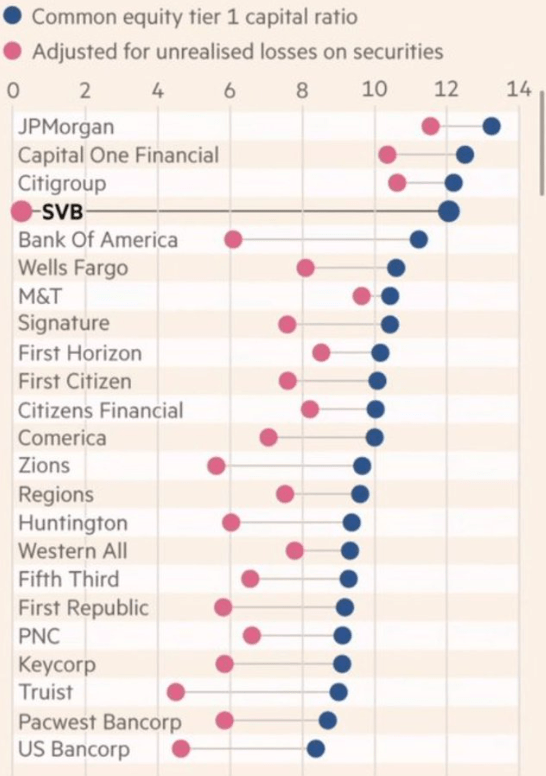

But here’s the thing — and this is the second difference between now and 2008. The extent of the losses varies widely from bank to bank. This time, the larger banks are in pretty good shape, because their holdings of government bonds formed only a modest share of their portfolios. In contrast, the smaller banks are in much bigger danger, because they had relatively few big-but-safe lending opportunities, which led them to put a greater fraction of their assets into government bonds.

You can see the pattern in this chart, published helpfully by the Financial Times. You can see the big banks at the top. They still have plenty of capital in their coffers, even after their bond losses — just look at the red dots. But the capital of the regional banks is much lower. (Although, um, please note Bank of America.)

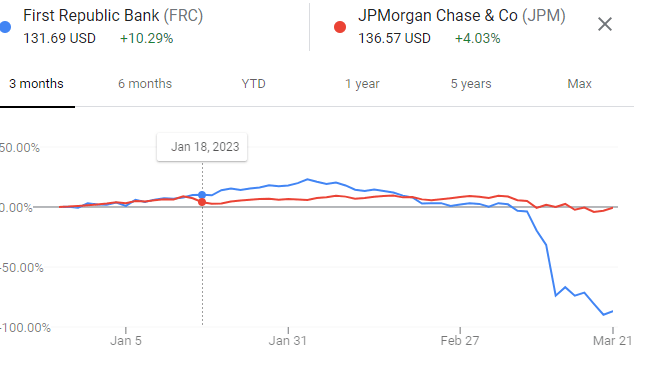

And markets know all this. They are making a big distinction between the sound and the vulnerable banks. That why the price of, say, First Republic bank has collapsed, while the price of JP Morgan has done precisely nothing.

So, there are two ways which this banking crisis is different. It’s a regional bank problem, not a systemic problem. And its all about interest rate risk, not credit risk.

It’s pretty obvious why the first point is good news: things would be far scarier if big banks like JP Morgan or Citibank were in trouble. But why is the second point good news? The answer is that once credit risk leads to defaults, nothing can be done. The banks have lost their money; the only thing left to do is to clean up the mess. But interest rate risk? Well, that can be undone! You see, if banks have lost money because rates on 10-year bonds have gone from 2 percent to 4 percent, all the Fed needs to do is to push bond rates back to 2 percent and the losses will disappear. Problem solved!

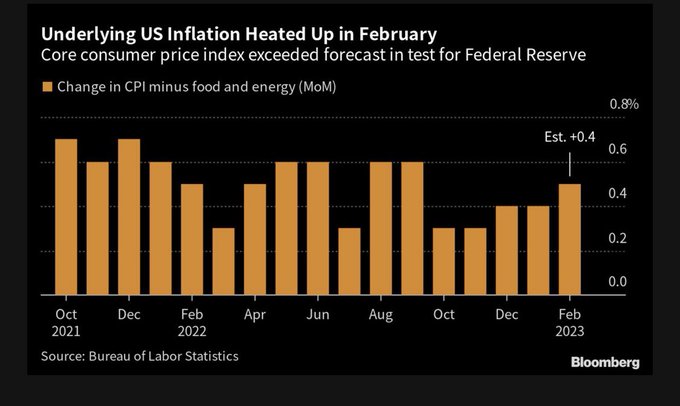

Of course, you know it can’t be that simple. And that brings us to the bad news, the major way in which the situation is worse than 2008. Back then, there wasn’t much inflation in the system. That gave the Fed enormous room to bring down interest rates to help revive the banking sector. This time, there is no such room, because inflation is far from under control. The chart below shows the problem. The Fed woulld like to get core inflation below 0.2 percent per month (roughly 2 1/2 percent per year). But inflation is running at double that level — and instead of falling, it has actually been rising in the past few months. That’s a problem.

Put another way: now, unlike 2008, there is a conflict between the Fed’s objectives of ensuring price stability and ensuring financial sector stability. That leaves the central bank between a rock and a hard place. Raise rates, cause more mark-to-market losses, and intensify the banking problems. Halt the rate increases and lose the fight against inflation.

For the moment, the Fed might be able to escape the dilemma. Markets expect that the Fed will today raise interest rates by 25 basis points to show it remains determined to curb inflation. At the same time, the Fed will probably take pains to point out that it has pulled back from the 50 basis point increase it was signalling earlier, because it is worried about the banking system.

But this fudge can only last so long. Ultimately, the Fed will need to make its priorities clear. Indeed, the Fed will have to give some hints today, because it will be releasing its interest rate forecasts. So, the markets will be able to see which path the Fed is planning to take.

Which way should it go?

It’s not obvious. Let’s say the Fed continues to raise interest rates and more banks go under. In principle, the Fed could decide that this is a cost worth paying. After all, the problem is not in the big banks; it’s at the smaller ones. But the smaller banks are not trivial. They play a key role in certain areas, providing two-thirds of the lending for commercial real estate and half of the lending for non-housing consumer loans. So, in practice the smaller banks can’t be abandoned.

Accordingly, let’s assume the Fed gives priority to stabilizing the banks. In that case, it would need to give up its fight against inflation. This would not go down well with the public. Not at all.

So perhaps the Fed could tackle the problems sequentially, focusing now on the banking crisis and later, say next year, on inflation? It sounds like a reasonable compromise. But it won’t work.

The problem is subtle, but very real. The longer the Fed allows inflation to continue, the more inflation becomes entrenched, thus requiring higher and higher interest rates to root out. But at the same time, raising interest rates becomes more and more difficult, because financial firms would have built their portfolios on the assumption the Fed will keep interest rates low to help the banks. As a result, raising rates would destroy these portfolios and precipitate the crisis that the Fed is trying to avoid.

This is not just a theoretical possibility. It has happened before. For most of the 1970s the Fed was too scared to tackle inflation. By the end of the decade, the public demanded action, forcing the Fed’s hand. So, Chairman Paul Volker tightened policy — and found to his horror that he needed to raise interest rates to 20 percent to restore price stability. Which in turn caused a financial crisis and a deep recession. Clearly, it would not be good to repeat that experiment.

Summing up:

- giving priority to price stability is a problem

- giving priority to financial stability is a problem

- tackling the two sequentially creates even greater problems

Great. Is there no way out? Actually, there is. The key is to separate banking policy from monetary policy. How can this be done?

Many people think that the Fed should provide banks with “liquidity” (i.e., cash), so that they can repay depositors who want their money. At some point, surely, the customers will come to their senses, bring their money back, and the crisis will be over. Right?

Wrong. The troubled banks aren’t actually facing a liquidity problem. After all, the portfolios of the troubled banks are full of government bonds, which they can easily sell, if depositors want their money back. The problem is that the bonds they had bought for $100 now only fetch $84 in the market. (Because when interest rates go up, bond prices go down.) So, if a customer wants to withdraw $100, the bank will be short $16. In other words, the problem is not liquidity; it is solvency.

That’s why the Fed announced a program week that effectively allows banks to swap their bonds for cash. The idea goes something like this. The bank can give a bond they bought for $100 to the Fed in return for $100 in cash. So, if a customer wants to withdraw $100 from the bank, the bank can just hand over the cash it got from the Fed.

Sounds great, doesn’t it?

But there’s a catch. The Fed isn’t going to hold that bond forever. If it did, it would lose $16 on the swap. So, the scheme calls for the swap to be reversed after one year, with the bank getting the bond back and the Fed getting $100 cash, plus interest.

In other words, the program isn’t solving the banks’ solvency problems. It is merely “kicking the can down the road” for one year. That is why it hasn’t succeeded in restoring confidence in the regional banks, whose deposits and share prices continue to fall.

There is ultimately only one way to solve this problem. The Fed needs to find a way to get capital into the regional banks.

But how can the Fed do this — from where would the capital come? In 2008, the shareholders of the major banks were willing to put in capital because these banks had a valuable business model: after all, they were the kings of global finance. In contrast, it’s not obvious that existing (or potential) shareholders want to put capital into smaller banks that have mismanaged their affairs. (See my previous post about the failings of SVB.)

Perhaps, then, the capital could come from the big banks, which might want to acquire some of the regional ones so they could expand their commercial real estate or other businesses. In fact, it seems they are indeed interested in at least some of these banks: that’s why there was a bit of a rally in share prices yesterday; there was speculation that some deals were in the works. But the deals are hardly done, since the FDIC is wary of letting the big banks get even bigger. See this really interesting article on the bidding for SVB.

Somehow, this problem needs to be solved. And quickly. Otherwise, the pressure to solve the solvency problem by distorting interest rates will become unbearable. And then the economy will be in an even bigger mess than it is today.

So, stay tuned. Watch the banks and watch the Fed. As Yogi used to say, “It ain’t over till its over”. And in the meantime, “You can observe a lot just by watching.”

Excellently written article. its always a delight to read your analysis/ opinions.

Ultimately i think its also question of viability. In US the no of banks are too many. in times like this they are bound to go under. there isn’t enough profitable opportunity available to sustain

LikeLike